Dec 7, 2023

How to Start Investing: A Comprehensive Guide for Beginners

Investing isn’t just for the wealthy; it’s a pathway to financial growth for everyone. Whether you’re a beginner with a very modest budget or someone looking to diversify their savings, understanding how to start investing is your first step towards financial empowerment.

In this article, you’ll learn:

- Decoding investing: What you need to know first

- How to get started investing

- Why investing is important

- When you should start investing

- The difference between active vs. passive investing

- Common questions about investing

Decoding investing: What you need to know first

Investing – it’s a word that might conjure images of high-flying stock traders, complex charts, and confusing terminology. But at its core, investing is simply about putting your money to work for you in a way that earns more money over time.

Why Invest? The primary reason is to grow your wealth. Essentially, it involves looking out for your future self. Whether saving for retirement, a down payment on a house, or your child’s education, investing is one of the best ways to reach these financial goals. Unlike putting your money in a savings account, investing offers the potential for higher returns, albeit with some level of risk.

How to get started investing

Investing means buying securities (which is an investment), like stocks, bonds, mutual funds, and exchange-traded funds (ETFs), to make money as they grow in value over time.

Investors generally create a portfolio made up of these various investments and often hold them for years or even decades. Traders, on the other hand, generally buy and sell investments rapidly to generate many small profits as prices rise and fall.

If the idea of day trading makes you sweat, rest assured: investing is generally much simpler and less stressful. Remember that investing should be a marathon, not a sprint. Here’s how to get started.

1. Define your investment goals

Learning how to invest starts with a crucial step: defining your investment goals. It’s about understanding why you want to invest and what you hope to achieve. Are you saving for a comfortable retirement, a down payment on a house, or your child’s education?

Defined goals help new investors stay focused and motivated, especially during market fluctuations. They act as a compass, guiding your investment decisions and helping you measure progress. Each goal will have a different time frame and risk profile.

At Stash, we believe in the power of goal-oriented investing. It’s not just about growing your wealth but aligning your investments with your life’s objectives. When you have clear goals that matter to you, you can tailor your investment strategy to match them.

2. Make sure you’re ready to invest

Before you start investing, you may want to first determine if you’re ready. Here are some indicators that the time may be right:

- Disposable income. If you can pay all your bills with a bit left over, it might be time to put your dollars to work. If you’re not currently budgeting, now is the perfect time to get started.

>>Learn more: How to make a budget - No high-interest debt. Let’s say you earn 5% on your investment, but you owe 18% interest on a credit card balance. That cancels out your return and then some, so paying down high-interest debt before you invest may be a good option.

>>Learn more: How to get out of debt - An emergency fund. Do you have three to six months of expenses in savings? If not, tying up all your extra cash in investments might force you to liquidate fast in case of an emergency, which may cause you to lose money on your investments.

>>Learn more: How to start emergency and rainy-day funds - Clear financial goals. Both investing and saving can be good ways to set aside money for the future; they each serve different functions. Setting goals and determining the right financial tools for meeting them lay a solid foundation.

>>Learn more: How to create your financial plan

Even if you have $1,000 to invest, it may be better to put that money toward things like high-interest debt and an emergency fund if those aren’t in place yet.

3. Set up your investment budget

If you’re ready to invest, the next step is to decide how much you can afford to invest. It doesn’t have to be a large sum; even small, regular contributions can grow significantly over time, thanks to compound interest.

In fact, with many online brokers, you can often get started investing with as little money as a dollar. While shares of stock and other securities can be costly, many brokerages sell them by the slice via fractional shares.

Once you start investing, you’ll likely want to keep adding money to your accounts, especially if you have long-term goals like retirement. Many experts recommend investing 10-20% of your income on an ongoing basis. But these are guidelines, not hard rules.

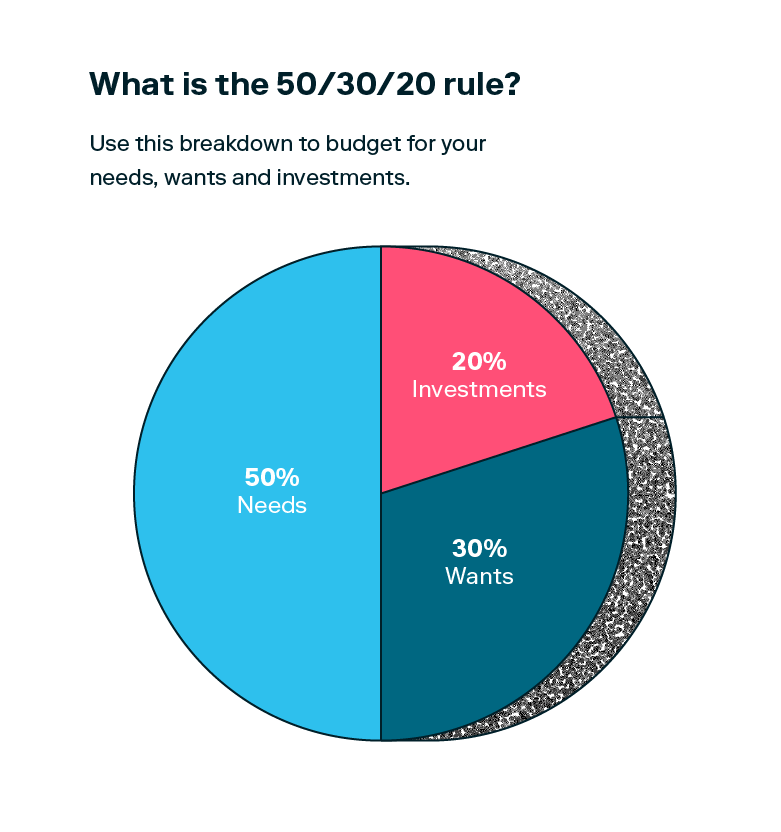

The 50/30/20 budgeting method, for example, allocates around 20% of your budget to savings and investments.

But for many people, investing 10-20% of your income might not be immediately practical. What matters most is starting early and investing consistently within your means. Even using a strategy like micro-investing can lead to significant growth. Use a compound interest calculator to see how your money could grow over time.

>>Learn more: How much you should be investing

| Tip: Start by saving 1% of your salary if that’s all you can afford now, and work your way up in 1% increments. Saving for retirement may feel like a luxury or impossibility, but any amount of savings is better than none. |

4. Choose the right investment account

The next pivotal step in your investing journey is opening an investment account, but it’s not just about picking any account. Your choice should be guided by the goals you’ve set.

For instance, if you’re saving for retirement, you might choose a tax-advantaged individual retirement account (IRA). If you’re saving up for your future dream house, you might consider a standard brokerage account.

There are several types of investment accounts to choose from.

- Taxable brokerage accounts. A brokerage account allows you to buy and sell virtually any investment. Adults can also create custodial accounts for children.

>>Learn more: How to open a brokerage account - Employer-sponsored retirement plans. This category includes 401(k), 403(b), SEP Individual Retirement Accounts (IRAs), and SIMPLE IRAs. Many workplaces offer an employer match, which is essentially free money for your retirement.

>>Learn more: Roth IRAs vs. 401(k)s - Individual retirement accounts (IRAs). If you don’t have an employer-sponsored plan, or if you want to invest more, a traditional or Roth IRA can help you save for retirement and reap tax advantages.

>>Learn more: Traditional vs. Roth IRAs - 529 education savings plan. Saving for your child’s education? A 529 savings plan may offer flexibility and tax advantages.

>>Learn more: Custodial accounts vs. 529 savings plans

5. Think about your risk tolerance

All investment involves risk, including the risk that you could lose money. But how much risk each person is comfortable with is very personal. Your age, income, financial goals, and other factors play a role. Investors typically sort risk tolerance into three categories:

- Conservative. A conservative investor values stability over the potential for higher investment returns. Asset allocation is likely to be 40% stocks and 60% bonds.

- Moderate. Moderate investors aim to balance stability with higher reward potential. Typically, they allocate 60% to stocks and 40% to bonds.

- Aggressive. Aggressive investors feel comfortable taking big risks and hope to earn big rewards. They usually allocate 80% to stocks and 20% to bonds.

It’s vital to know your comfort level. Are you okay with high-risk, high-reward options, or do you prefer a safer, steady growth approach? Are you getting closer to retirement age, or do you have decades to go? Your risk tolerance will influence the types of investments you choose, balancing potential gains with the possibility of losses.

>>Learn more: Determine your risk profile

6. Choose your investments

In this next step, you’ll choose investments based on your goals and risk tolerance. There are many types of stock market investments available; most everyday investors put their money in stocks, bonds, mutual funds, or ETFs. Cryptocurrency is also becoming a popular investment option, although it is a very risky investment. Additionally, you can even invest in real estate through a real estate investment trust (REIT).

For beginners, index funds and mutual funds can be a great way to start as they can offer built-in diversification and lower risk. Stash can guide you in choosing investments that match your financial objectives and risk profile.

| Investment type | What it is | Volatility | Performance profile |

|---|---|---|---|

| Stock | A piece of ownership in a company | Generally higher | Value tends to rise and fall; may trend up over the long term. May pay dividends. |

| Bond | A loan to a company or government paid back with interest | Usually lower | Growth tends to be slow and steady. |

| Mutual fund | A basket of investments, like stocks, bonds, and other securities | Varies | Profile reflects fund composition. Offers some diversification. May pay dividends. |

| Exchange-traded fund (ETFs) | A basket of investments, like stocks, bonds, and other securities | Usually lower, as many are passive index funds | Profile reflects fund composition. Offers some diversification. May pay dividends. |

| Cryptocurrency | A decentralized currency with no set value | Usually very high | Price spikes and dips rapidly. |

The table above reflects general information on volatility and performance profiles. But there is tremendous variation within each investment type. Value stocks, for example, tend to be relatively stable, while “junk bonds” can be quite risky. That’s why it’s important to research stocks, funds, and any other investment options before investing.

>>Learn more: Different types of investments

7. Decide your investment approach – DIY or robo-advisors

As you learn how to start investing, another critical decision you’ll make is whether to manage your investments yourself (DIY) or use a robo-advisor. Each approach has its benefits and considerations.

DIY investing allows you full control over your investment choices. You can select individual stocks, bonds, ETFs, and other assets based on your research and preferences.

It requires a commitment to learning about financial markets, investment strategies, and how to monitor your portfolio. It’s ideal for those who have a keen interest in financial markets and want to be actively involved in managing their investments.

Robo-advisors use algorithms to manage your investments based on your goals and risk tolerance. They automatically allocate your funds across various assets and rebalance your portfolio as needed.

Automated investing is great for beginners or those who prefer a hands-off approach. It eliminates the need for extensive market knowledge and ongoing portfolio management, saving you time and effort.

8. Monitor and adjust your investments

Once you’ve laid the groundwork and made your investment choices, you’re officially investing. You no longer have to figure out how to start because you’re doing the thing.

But remember — investing isn’t a set-it-and-forget-it activity. Regularly review your investments to ensure they align with your goals and make adjustments as needed. Market conditions change, and so might your financial situation or goals. Consult a Certified Financial Planner for personalized advice on how to use investment funds to reach your financial goals.

When you first start investing, it can feel overwhelming. But it doesn’t have to be complicated to begin putting your money to work. The Stash Way® can help: it’s all about investing what you can afford on a regular basis, building a diversified portfolio, and investing for long-term growth.

>>Learn more: How you can diversify your portfolio in 2024

Why is investing important?

Many experts agree that investing is a critical component of a brighter financial future. About 61% of Americans own stock (Gallup, 2023), and many invest in other types of investments as well. Here are some of the most common reasons people invest:

- Retirement. In 2022, 72% of non-retired Americans had some retirement savings, and many put those dollars into investment accounts. Investing could help your nest egg grow faster than saving alone (Federal Reserve, 2023).

>>Learn more: Calculate how much you’ll need to retire - Combating inflation. Money loses buying power over time: an item that cost $100 in 1950 would cost over $1,276.64 today in 2023. Investing can be particularly important during inflationary times to preserve and grow the purchasing power of your money.

>>Learn more: How to combat inflation - Lowering tax burden. Retirement and college savings accounts offer tax advantages that could lower your taxable income, and some investment profits are taxed at the lower capital gains rate of 0-15%.

>>Learn more: How taxes on stocks work - Growing wealth through passive income. Investing puts your dollars to work for you. You might earn passive income through dividends, as well as returns when you sell securities that have increased in value.

>>Learn more: Passive income streams

How early should you start investing?

As a general rule, the sooner you start investing, the greater your earning potential. How? The power of compounding.

Imagine you invest $100 and earn a 5% return annually. In the first year, you’d earn $5. When you re-invest those earnings, you’d earn interest on $105 the next year, for a return of $5.25. Every time your money makes money that you re-invest, it increases your balance, as well as the return on that balance.

The longer your money compounds, the greater the effect. Let’s say you start with $100 and contribute $25 a month for 20 years, earning an average rate of 5%. After 20 years, you’d have deposited $6,100 and your balance would be over $10,000. And after 50 years, you’d have contributed $15,100 and your balance would be almost $64,000.

The moral of the story is clear: there is no right age to start investing. But the earlier you begin, the more time your money has to grow. Think long-term and harness the power of compounding to build wealth.

>>Learn more: Calculate compounding over time

What’s the difference between active vs. passive investing?

In the world of investing, there’s a place for every kind of investor. Are you a hands-on or hands-off investor? Each approach comes with risks and benefits.

Hands-on, active investors tend to focus on short-term gains; they usually spend substantial time maintaining their portfolios and trade more frequently. Active investors may also try to beat the stock market by choosing specific stocks that may outperform leading indexes like the S&P 500.

But even professional fund managers don’t beat the market reliably. Active investing can be a higher risk and involve more account fees due to the frequency of trading.

Passive, hands-off investors usually practice a buy-and-hold investing strategy: they hold their investments for long periods of time, seeking a long-term return. They frequently invest in index funds that aim to mimic the performance of the market overall and keep them for a long time.

Passive investing is often recommended for long-term goals like building wealth for retirement. Even Warren Buffett, one of the most successful investors, emphasizes the importance of long-term, value-driven investing strategies.

| Active investing (hands-on) | Passive investing (hands-off) |

|---|---|

| High volume of trades | Buy-and-hold approach |

| Hands-on portfolio management | Less frequent portfolio management |

| Tends to focus on individual securities | Tends to focus on a diversified portfolio |

| Higher risk | Lower risk |

| Geared toward short-term returns | Geared toward long-term returns |

>>Learn more: How passive investing works

Common Questions About Investing

Is investing in the stock market risky?

Investing in stocks always involves risk. While you can make money by investing in stocks, bonds, funds, and other securities, you can also lose money, especially if your investments lose value. It’s a good idea to diversify and do careful research before you purchase securities, so you can reduce your risk.

How do I invest money in the stock market?

You can invest in the stock market by purchasing stocks, bonds, mutual funds, and exchange-traded funds (ETFs), as well as other securities. You can make these purchases by setting up an investment account with a brokerage, either online or through an investment app. Use the steps in this article to learn how to start investing.

How much money do you need to invest in stocks?

You may think you need a large sum of money to start investing in order to buy pricey stocks or other investments. But you can crack into the investing world with as little as $1 thanks to fractional shares. As their name implies, these are fractions of full shares that can help you start investing, sometimes with just a few dollars.

Is $100 enough to start investing?

Absolutely, $100 is enough to start investing. Many online brokers and robo-advisors offer low or no minimum investment requirements, making it accessible for beginners. Also, options like fractional shares allow you to invest in high-value stocks with smaller amounts of money. Starting with what you have, even if it’s $100, is a great step towards building your investment portfolio.

What is the difference between trading and investing?

Trading is the process of buying and selling individual stocks, which usually takes place over the short term. Investing generally implies buying stocks or bonds and holding onto them over a longer period of time.

Investing made easy.

Start today with any dollar amount.

Subscribe

All episodes are available now. You can listen to Teach Me How to Money right here on our site, and via the podcast apps below.

Written by

Cassidy Horton

Cassidy Horton is a finance writer with over five years of experience. She holds an MBA and a bachelor's in public relations from Georgia Southern University and has worked with top finance brands like Forbes Advisor, NerdWallet, Consumer Affairs, USA TODAY Blueprint, MarketWatch, Money, The Balance, and more. Similar to Stash, Cassidy believes everyone should have equal access to financial education and the resources they need to achieve their life goals. She is also the founder of Money Hungry Freelancers, a finance platform dedicated to helping other freelancers build a strong financial foundation.

1Example is a hypothetical illustration of mathematical principles, and is not a prediction or projection of performance of an investment or investment strategy

*For Securities priced over $1,000, purchase of fractional shares starts at $0.05.

Stash does not monitor whether a customer is eligible for a particular type of IRA, or a tax deduction, or if a reduced contribution limit applies to a customer. These are based on a customer’s individual circumstances. You should consult with a tax advisor.

This material has been distributed for informational and educational purposes only and is not intended as tax advice. Consult with your tax professional.

Related Articles

15 Largest AI Companies in 2024

The 12 Largest Cannabis Companies in 2024

What Is a Traditional IRA?

Saving vs. Investing: 2 Ways to Reach Your Financial Goals

How To Invest in the S&P 500: A Beginner’s Guide for 2024

Stock Market Holidays 2024

By using this website you agree to our Terms of Use and Privacy Policy. To begin investing on Stash, you must be approved from an account verification perspective and open a brokerage account.