Apr 17, 2023

17 Best Investing Apps for Beginners in 2023

If you’re like most Americans, you reach for your smartphone dozens of times a day to catch up on the news, touch base with friends and family, and manage your personal life. You may even check your bank balance or use an app to pay a buddy back for the coffee they bought you yesterday.

That computer in your pocket can come in handy when it’s time to make investment decisions, too. Investing isn’t just for high-net-worth individuals who meet face-to-face with financial advisors to put a lot of money in the market. Discount and online brokerages have opened the door to new investors looking to get their feet wet.

The smartphone offers the next chapter in this story: micro-investing apps are designed for investors who don’t have a ton of money to invest right away but want to add incrementally to their savings over time.

Before you take the plunge, it’s important to think clearly about why you’re investing and what you hope to get out of an investing app. Instead of diving into the detailed specifics of a specific app, start by thinking about the features and services that make the most sense for you. Then you’ll be able to narrow the field of apps.

Stay with us as we break down the 17 best investing apps for beginners, why we like them so much, and how they can benefit your financial future.

- Stash

- Fidelity Investments

- Acorns

- Robinhood

- Betterment

- Wealthfront

- Charles Schwab

- Ellevest

- SoFi Invest

- Public

- TD Ameritrade

- Ally Invest

- Webull

- Round

- Greenlight Max

- UNest

- Invstr

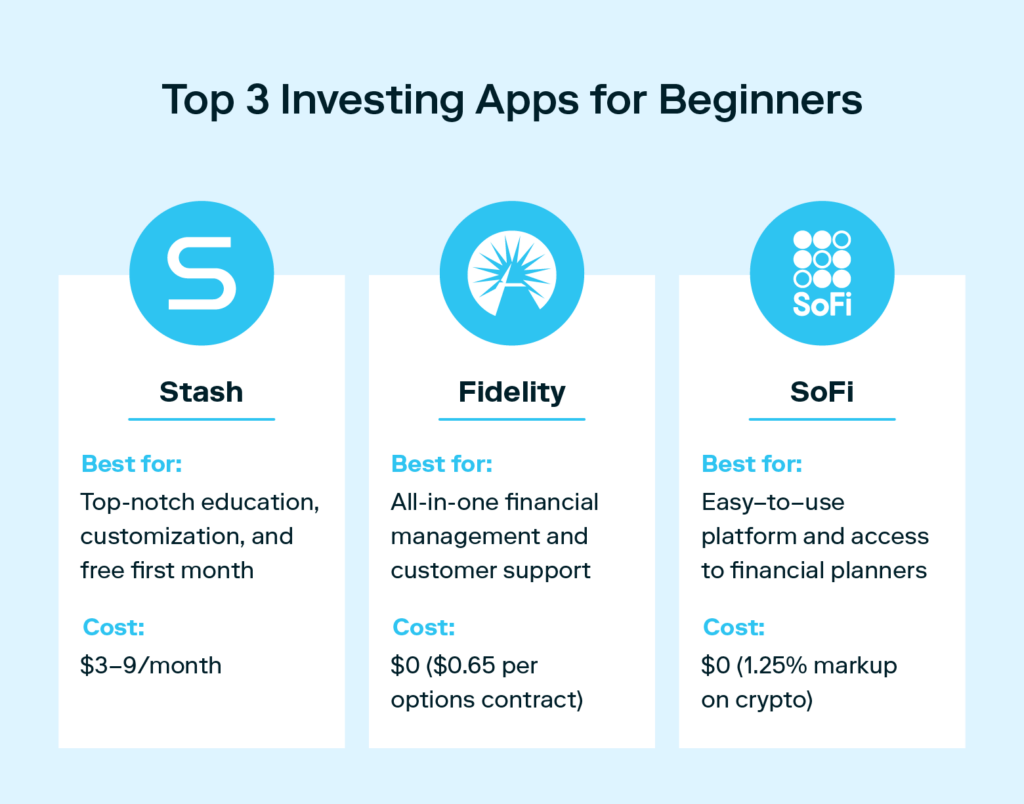

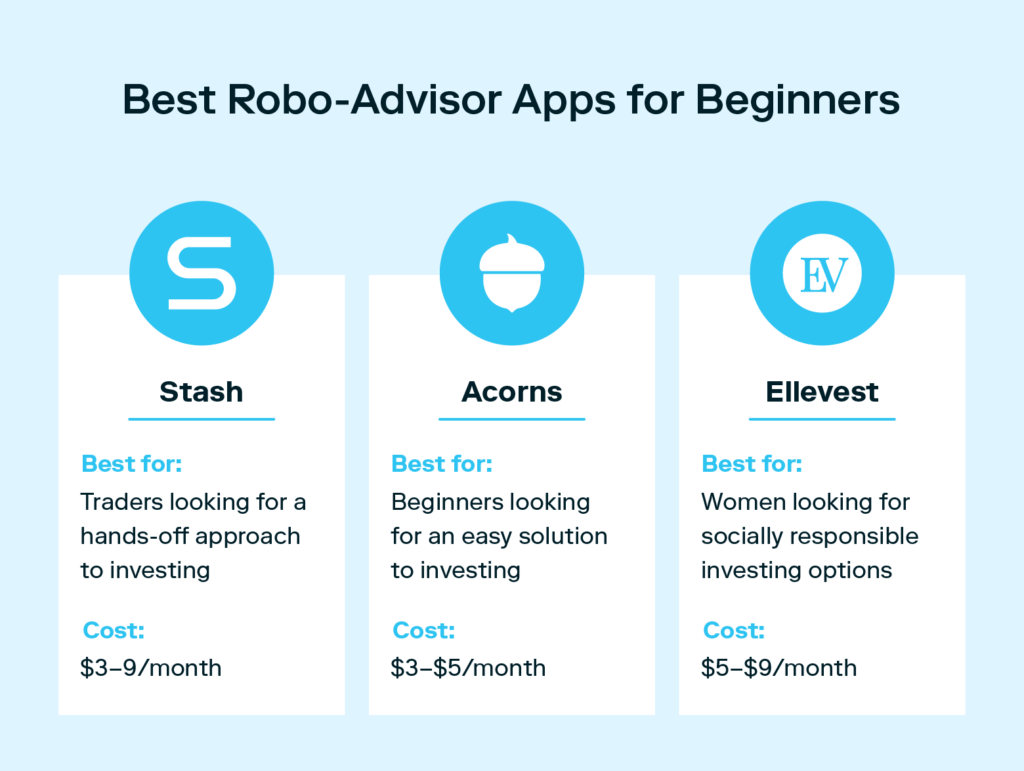

1. Stash

Best for: beginner investors who want personalized investing advice and control of their investments

Stash is a comprehensive investing and personal finance app for new investors wanting to build wealth. We educate our users so they can make smart investment decisions, like investing regularly, diversifying their portfolio, and thinking long-term. Investors get out of Stash what they want, whether that’s making DIY or automated investments.

Our basic subscription—Stash Growth—offers personal, smart, and retirement portfolios, banking access, and $1,000 in life insurance through Avibra.1 This plan is best for growing personal finances. The next plan—Stash+—offers everything within the basic plan, plus investing portfolios for kids (custodial accounts) and $10,000 in life insurance.

Cost: $3-$9/month

| Pros | Cons |

|---|---|

| Affordable investing, as little as $0.01 | Only four trading windows per day |

| Earn up to 3% in stock rewards with the stock-back debit card | No automated IRA investing |

| Ability to choose individual stocks and ETFs from a wide range | |

| Ability to set up recurring transactions | |

| No add-on commission fees |

Your portfolio, your way.

Build a personalized portfolio from thousands of stocks & ETFs.

2. Fidelity Investments

Best for: beginner and experienced traders wanting all their finances in one place

Fidelity offers a well-rounded brokerage app that features checking and savings accounts, credit card accounts, investment accounts, IRAs, bill paying, and more. Under one roof, you can essentially handle all of your finances if that’s what you’d like.

Cost: $0 per trades of mutual funds, ETFs, stock, or options plus $0.65 per contract with options trading

| Pros | Cons |

|---|---|

| Wide investment selection | High broker fees |

| No commission fees | Slow to allow crypto trading |

| Known for their customer service | Only offers access to Bitcoin and Ethereum |

| Educational resources to help new investors make informed decisions |

3. Acorns

Best for: people who know they should be investing but need someone to do it for them

Acorns is another easy-to-use investing and personal finance app great for beginners looking for an app to take care of all the work of investing. Their well-known “Invest spare change” function rounds up debit or credit card purchases to the nearest dollar and invests the difference into ETFs within a user’s portfolio. This system helps users build better saving habits.

If you’re looking for an app to set up once and let it run your investment portfolio, Acorns might be for you.

Cost: $3–$5/month

| Pro | Cons |

|---|---|

| Real-time Round-Ups | Unable to choose individual stocks and securities |

| Recurring investments as low as $5/day, week, or month | Limited customization |

| Cash back perks at 450 retailers | High fees for accounts with small balances |

| Banking access with 55,000+ fee-free ATMs |

4. Robinhood

Best for: active, short-term investors who don’t need much support

The Robinhood trading app allows trades of stocks, ETFs, cryptocurrency, and other securities at an affordable price. This app works best for active investors and traders.

Robinhood appeals to beginner investors with its intuitive platform, low cost, and basic features. However, users have total control of their investments but have little access to education and customer service within the app. With limited support, it’s easy for novice investors to enter trades they don’t understand.

Cost: $0 to $5/month

| Pros | Cons |

|---|---|

| Unlimited immediate trades | Limited educational resources |

| Tax savings | Limited customer support |

| No commission fees | Trading fees vary by investment |

| No mutual funds access |

5. Betterment

Best for: new investors with lower balances looking for an app to do the heavy lifting

Betterment is a popular robo-advisor app that lets users select their risk tolerance and return goals. It makes investments so the users don’t have to think about it—which can be enticing for those who’ve never invested.

Cost: $4/month or 0.25% annual fee for investing, 1% plus trading expenses for crypto trading

| Pros | Cons |

|---|---|

| Automated investing based on users’ risk tolerance and goals | No direct indexing |

| Premium advice on tax information in regards to investing | Premium plan’s balance requirement is $100,000 |

| Cash management account available |

6. Wealthfront

Best for: novice investors looking for advice and planning in regards to saving money

Another robo-advisor, Wealthfront is well known for its goal planning tool. For beginner investors, Wealthfront has fallen behind its competitor Betterment since it’s a digital-only service with no human advisors and requires a high minimum balance.

But Wealthfront is picking up the pace in other areas—users can now invest in stocks and crypto (through Grayscale Bitcoin Trust and the Grayscale Ethereum Trust) easily on the app.

Wealthfront’s crypto trading opportunities come with limits, though. Users only have access to crypto indirectly, and crypto trades are not available in Wealthfront’s daily tax-loss harvesting—a strategy investors use to cut capital gains taxes by selling other investments.

Cost: 0.25% advisory fee

| Pros | Cons |

|---|---|

| Automatic rebalancing | $500 balance minimum |

| Tax-loss harvesting (crypto not included) | Customer support is limited |

| Digital wealth planning tool | Indirect cryptocurrency investing |

| Access to 529 accounts |

7. Charles Schwab

Best for: all investors—from beginner investors to stock trading experts

As a full-service broker, Charles Schwab attracts all levels of investors with its established reputation, three different platforms, and a wide array of tools and research. Investors can access stocks, ETFs, indirect crypto trading, and more.

Cost: $0 per trade of mutual funds, ETFs, stock, or options plus $0.65 per contract

| Pros | Cons |

|---|---|

| No commission fees | Lower selection of fractional shares compared to competitors |

| One of the largest and most trusted brokerage platforms | Indirect cryptocurrency investing |

| Known for their customer service |

8. Ellevest

Best for: women looking for socially responsible investing options

Ellevest is a women-founded financial organization made for other women, though anyone can invest on the app. The goal is to help women feel confident in investing by providing education and support. Ellevest also offers socially responsible investing (SRI), an investment strategy that results in financial returns and positive social change.

Beyond investing, users can also access financial planning, wealth management, and 401(k) rollover services.

Cost: $5–$9/month

| Pros | Cons |

|---|---|

| A robo-advisor with human advisors available | Recently removed the cash management account function |

| Multitude of learning opportunities: one-on-one coaching, workshops, and email education | No tax-loss harvesting |

| Flat fee price structure that doesn’t increase if your assets grow | More limited investment selection compared to competitors |

9. SoFi Invest

Best for: beginners looking for an affordable, easy-to-use platform

It costs just $1 to get started with SoFi Invest, regardless of whether you’re investing that dollar yourself or utilizing SoFi’s automated investing service. The personal finance app is organized and straightforward, landing it on our list of best investing apps for beginners. Users have access to stocks, ETFs, crypto, and more.

Cost: $0 except 1.25% for crypto trading

| Pros | Cons |

|---|---|

| No commission fees | 1.25% markup on cryptocurrency trading |

| Can start investing with as little as $1 | No tax-loss harvesting |

| Free access to financial planners |

Automated investing, simplified.

Let us invest for you with Smart Portfolio.

10. Public

Best for: new investors looking to chat with other traders in the same boat

Public makes investing social—it’s a social network meets brokerage. While users trade stocks and ETFs, they can also engage with one another on the Public feed to learn more about investing. One of the biggest downsides of Public’s app is the markup on crypto trades.

Cost: $0-$10 (depending on the plan)

| Pros | Cons |

|---|---|

| Educational content and group chats | 1%–2% markup on cryptocurrency trading |

| No commission fees | Semiannual $5 inactivity fee on accounts with less than $20 |

11. TD Ameritrade

Best for: beginner and experienced investors

Charles Schwab acquired TD Ameritrade in 2020. The two brokerages have very similar features and platforms, but the biggest differences are TD Ameritrade is available only in the U.S. and Canada and doesn’t offer fractional shares.

Cost: $0 per trade of mutual funds, ETFs, stock, or options plus $0.65 per contract with options trading

| Pros | Cons |

|---|---|

| No commission fees or account minimums | No fractional shares |

| Wide investment selection | No direct access to crypto trading |

| Free educational content |

12. Ally Invest

Best for: novice investors wanting a fresh, all-encompassing experience

Ally Invest offers both self-directed and automated investing. In addition to investing, Ally also offers checking and savings accounts, credit cards, retirement accounts, loans for homes, auto, and personal. The all-in-one financial management makes Ally a good investing app for beginners.

In February 2023, Ally cut their $9.95 mutual funds trading fee, but their features favor those with deeper pockets. Ally’s robo portfolios have a $100 investment minimum, and they offer wealth management for high-value accounts of $100,000 or more.

Cost: $0 per trade of mutual funds, ETFs, stocks, or options plus $0.50 per options trade contract

| Pros | Cons |

|---|---|

| No commission fees or account minimums | $100 minimum for automated investments |

| Offers foreign stocks | No fractional shares |

| High-quality market analysis tools | Third-party research |

| No direct access to crypto trading |

13. Webull

Best for: a younger generation of investors with some knowledge

Webull is a high-quality trading platform built with a mobile-first generation in mind. It offers extensive data visualization tools like charts and a stock screener to aid investment decisions. However, the educational content is sparse and secondhand, so beginners who do best with Webull come to the table with some prior knowledge on investing terms.

Unlike some apps, Webull offers zero commission fees on all trade types and amounts.

Cost: $0, with $0.55 per contract for some index option trades

| Pros | Cons |

|---|---|

| No commission fees | Lacks unique educational content |

| Easy to use | No access to mutual funds |

| Access to crypto trading | No cash management accounts |

14. Round

Best for: new investors needing guidance or investors with large investment capital

Round is another investing app that provides the advice of human, financial advisors instead of relying on an algorithm. Having human help appeals to investors who can’t manage their investments for themselves, whether that’s because of time constraints or inexperience. Round offers a private manager on accounts with large balances of over $100,000.

Cost: 0.5% annual fee

| Pros | Cons |

|---|---|

| Investments managed by financial advisors | No retirement planning |

| Top-tier analysis tools | Not available on Android |

| No fees if no returns | $500 investment minimum |

15. Greenlight Max

Best for: children interested in investing and parents who want to teach their children about money

This one is for the parents in the crowd—Greenlight. At its core, Greenlight is a debit card for kids. The aim is to build good financial habits and set savings goals. Parents can direct deposit allowance money into their child’s account and set up investments to build long-term wealth for their child’s future. The app offers parental controls where parents approve of trades of stocks and ETFs. Investing is not available on Greenlight’s lower tiers.

Cost: $7.98/month

| Pros | Cons |

|---|---|

| Offers educational games and quizzes | More expensive than other debit cards for children |

| Educational content from experts written for kids | One primary account holder—not set up for multiple parents to manage the account |

| 4,000+ stocks and ETFs available |

16. UNest

Best for: parents who want to invest in their children’s future but don’t have the time or knowledge to manage portfolios themselves

The UNest app allows parents and guardians to open custodial investment accounts for their children. UNest offers the two most common types of custodial accounts: Uniform Transfers to Minors Act (UTMA) accounts and Uniform Gift to Minors Act (UGMA) accounts. Unlike Greenlight, UNest doesn’t offer cash management accounts.

As a robo-advisor, UNest offers pre-built portfolios for parents based on risk tolerance and financial goals. It’s a good option for parents looking for an easy way to invest for their children without usage restrictions. When the child reaches adulthood, they can use the funds for education, reinvest it, or just as a nest egg to start their adult life with (unlike 529 Plans which are strictly for education).

Cost: $4.99/month for UNest Core and $5.98/month for UNest Plus, plus $25 monthly minimum contributions

| Pros | Cons |

|---|---|

| No commission fees | High fees for accounts with small balances |

| Tax savings with kiddie tax | Monthly contribution requirement |

| Friends and family can contribute to the accounts | Could impact financial aid as balances count as income |

| Rewards when parents shop at 150+ brand partners like Disney+ and DoorDash | No direct cryptocurrency access (third-party through Apex Crypto) |

17. Invstr

Best for: beginners who want to practice before spending money on investing

Invstr is a unique app with several appealing features, but they come at a cost. The free Invstr+ version offers basic investing and personal banking capabilities. The paid Invstr Pro version opens up access to the Portfolio Builder tool, which provides personalized investment recommendations, and Fantasy Finance, Invstr’s gaming product.

Invstr is one of the only well-known investing apps with real-life and investing games. In Fantasy Finance, each player receives $1,000,000 in virtual funds to play against friends, pick stocks, and trade crypto in simulation.

Winners still receive prizes, but prizes are typically Amazon gift cards. Users can play for fun or play for practice and education.

Invstr also has an app for kids and teens called Invstr JR. It’s most similar to Greenlight.

Cost: $0 for Invstr+, $3.99/month for Invstr Pro, plus 1.5% for crypto trading. $5 minimum investment.

| Pros | Cons |

|---|---|

| No commission fees | 1.5% markup on cryptocurrency trading |

| Allows fractional shares | Limited access to customer support |

| Access to third-party insurance for home, auto, pet, life, and renters’ policies | Paid version only has access to the Portfolio Builder |

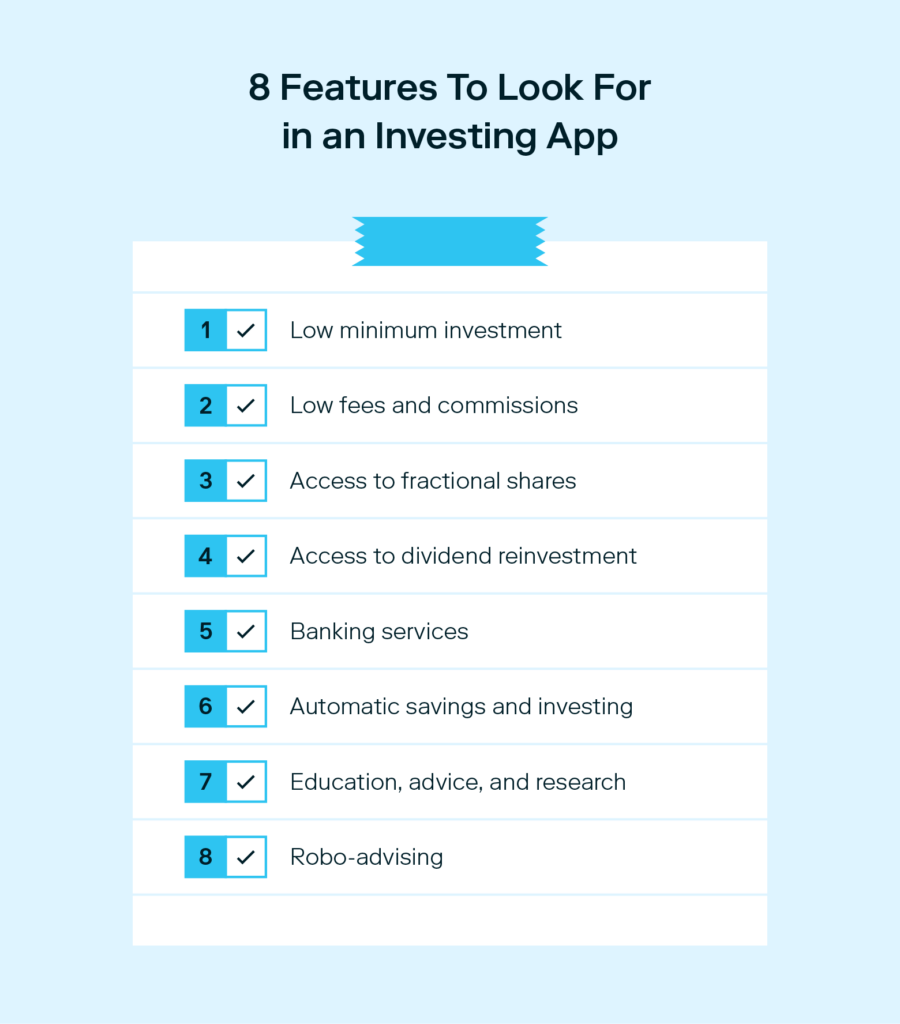

What to look for in an investing app

Beginner-friendly micro-investing apps tend to focus on two areas: education and access to the markets. Education guides investors through the process of building and managing their portfolios. For most apps, the education component provides information and background on how the markets work.

Many apps offer lower fees or investment minimums to start an account. This allows beginners to invest on a scale that works for limited budgets.

These apps aim to provide a mix of comfort and convenience. If you wind up tossing and turning all night, worrying about how your money is doing, the app is not doing its job. Here are some features that could help you sleep better at night.

Low minimum investment

These days, you should have no problem finding a reliable app with a required minimum investment in the single digits. Every great investor has to start somewhere, and you should be able to find a way to begin investing with as little as $1.

Fees and commissions

Historically, Wall Street has charged clients fees each time they buy or sell stock. Some of today’s micro-investing apps do the opposite, typically offering trades without any fee at all.

While free trades may look attractive, you often get what you pay for. So read the fine print: low fees often involve a tradeoff in the level of service an investor receives. For example, a small monthly fee could pay off in the form of useful guidance and flexibility.

In many cases, your fees will decrease as your account balance grows. One note of caution: for investors starting small, flat fees can outweigh percentage-based fees that mutual funds typically charge, so it pays to calculate the fees you’ll actually pay.

Fractional shares and dividend reinvestment

Maybe you want to make a play on Amazon stock but don’t want to fork over more than $2,000 for a single share. Many apps will allow you to purchase a fraction of a share. This is a great way to dip your toes in the market before you jump into it.

Some companies pay out dividends—a distribution of the company’s earnings.

If you buy a stock that pays periodic dividends on your shares, you can use those dividends to automatically purchase more shares of the stock. This feature is known as a dividend reinvestment plan, or DRIP, and was once traditionally available only through the company offering the stock. Many apps allow you to reinvest dividends automatically.

Links to banking services

New apps may offer a wide range of financial services associated with investing in the stock or bond market. Some will allow you to directly link your external bank or credit card accounts with your trading account, while other services allow you to do your banking through the app.

The app might include attractive options such as branded debit cards, individual retirement accounts (IRAs), or custodial accounts that adults can open on behalf of a minor. When considering these perks, think about how attached you are to your current bank and whether moving to app-based banking fits your day-to-day, real-world life.

If you like looking a teller in the eye, or if using an ATM will require an additional fee, you may be better off sticking with your existing bank accounts.

Periodic savings

Many apps offer ways to set up regular transfers from users’ bank accounts to their savings or investment accounts held through the app. These incoming transfers can be automatically applied to a specific investment or set aside to earn interest until the user decides on an investment.

Education and advice

This is a huge part of the value of many apps. Beginning investors can benefit greatly from educational resources ranging from a glossary that explains basic stock market terms, to daily market commentary, to more sophisticated research on specific companies and industries.

Some allow users to read up on the importance of U.S. Treasury bonds’ yield curve or to listen to a podcast on emerging markets. Some apps have developed their own versions of investing games to acquaint novice investors with the ups and downs of the markets. These tools allow users to compete in investing competitions with friends, using virtual money, before getting into the real thing.

Robo-advising

Robo-advising provides the sort of financial guidance that a broker would give. Robo-advisors use an algorithm to offer investing advice based on certain parameters. Since there’s no human interaction involved, they tend to provide that advice for a lower fee than a financial advisor would charge.

Micro-investing apps tend to use the term “robo-advising” to refer to the bundling of stocks or investments to fit a specific theme. The possibilities are endless and often structure around your own personal interests. For example, themes can include food, travel, or socially responsible investing.

Investing made easy.

Start today with any dollar amount.

Best investing apps for beginners FAQ

Have more questions about finding the best investing apps for beginners? Let us help.

What are good investments for beginners to invest $1,000?

Exchange-traded funds (ETFs) make good first investments for beginners with smaller sums of money, like $1,000. ETFs carry built-in diversification, making them an affordable investment. IRAs also make good investments for beginners since they build wealth for retirement.

What investments can you trade through an app?

Online broker apps allow trading of the standard investment types—ETFs, stocks, bonds, cryptocurrency, and mutual funds.

How much money do you need to start investing?

It’s possible to start investing on an app for as little as $1. Many investing apps have no balance requirements after the first investment.

What is the easiest trading app for beginners?

When looking for an easy investing app for beginners, you want an intuitive interface, educational resources, and customer support. Stash, Acorns, and SoFi are three of the best trading apps for beginners, as they tick each of those requirements.

What is the best investing app for beginners?

However you take that first step into the world of investing, you’ll probably get better results if your investment is part of a broader, integrated approach to your financial well-being. Your smartphone can be the central place for that approach, with the right apps for each component of your plan, including your micro-investing platform.

A budgeting app can get your spending under control, while a debt management app can help you formulate a reliable and feasible plan for eliminating personal debt. Credit apps can track your credit rating and alert you of any red flags that you might otherwise miss.

Countless apps fit those descriptions, so it could take some looking to find the right one for you. Keep in mind that everybody’s circumstances are different, so there may not be one app that perfectly fits your needs.

With a bit of research, discipline, and self-awareness, you can find the mix that works best for you. Stick with it, find out what works, and you’ll be on your way before you know it.

As you do your research, consider Stash, which includes education to help you start investing, fractional shares to help you start small, Portfolio Builder to help you create a customized portfolio, and many of the other features mentioned above.

With Stash, you can start investing with any dollar amount today.

Methodology:

To compile this list of investing apps for you, Stash evaluated brokers and robo-advisors based on features that matter most to beginner investors, such as:

- Low fees and balance requirements,

- Available education,

- Ease of use,

- Variety of trading options, and

- Customer support.

Subscribe

All episodes are available now. You can listen to Teach Me How to Money right here on our site, and via the podcast apps below.

Written by

Team Stash

1 Group life insurance coverage provided through Avibra, Inc. Stash is a paid partner of Avibra. Only individuals who opened Stash accounts after 11/6/20, aged 18-54 and who are residents of one of the 50 U.S. states or DC are eligible for group life insurance coverage, subject to availability. Individuals with certain pre-existing medical conditions may not be eligible for the full coverage above, but may instead receive less coverage. All insurance products are subject to state availability, issue limitations and contractual terms and conditions, any of which may change at any time and without notice. Please see Terms and Conditions for full details. Stash may receive compensation from business partners in connection with certain promotions in which Stash refers clients to such partners for the purchase of non-investment consumer products or services. Clients are, however, not required to purchase the products and services Stash promotes.

2 Limitations apply; 3% Stock-Back rewards available only for qualified bonus merchants on Stash+. Stash Banking services provided by Stride Bank, N.A., Member FDIC. The Stash Stock-Back® Debit Mastercard® is issued by Stride Bank pursuant to license from Mastercard International. Mastercard and the circles design are registered trademarks of Mastercard International Incorporated. Any earned stock rewards will be held in your Stash Invest account. Investment products and services provided by Stash Investments LLC, not Stride Bank, and are Not FDIC Insured, Not Bank Guaranteed, and May Lose Value. In order for a user to be eligible for a Stash banking account, they must also have opened a taxable brokerage account on Stash. All rewards earned through use of the Stash Stock-Back® Debit Mastercard® will be fulfilled by Stash Investments LLC. You will bear the standard fees and expenses reflected in the pricing of the investments that you earn, plus fees for various ancillary services charged by Stash. In order to earn stock in the program, the Stash Stock-Back® Debit Mastercard must be used to make a qualifying purchase. What doesn’t count: Cash withdrawals, money orders, prepaid cards, and P2P payment. If you make a qualifying purchase at a merchant that is not publicly traded or otherwise available on Stash, you will receive a stock reward in an ETF or other investment of your choice from a list of companies available on Stash. 1% Stock-Back® rewards are subject to terms and conditions. Stock rewards that are paid to participating customers via the Stash Stock Back program, are Not FDIC Insured, Not Bank Guaranteed, and May Lose Value. Stash reserves the right to amend this program and the terms and conditions thereof and/or cancel this program at any time, for any reason, upon notice to you. See Terms and Conditions for more details.

Investment advisory services offered by Stash Investments LLC, an SEC registered investment advisor. Investing involves risk and investments may lose value. Ancillary fees charged by Stash and/or its custodian are not included in the subscription fee.

Related Articles

15 Largest AI Companies in 2024

The 12 Largest Cannabis Companies in 2024

What Is a Traditional IRA?

Saving vs. Investing: 2 Ways to Reach Your Financial Goals

How To Invest in the S&P 500: A Beginner’s Guide for 2024

Stock Market Holidays 2024

By using this website you agree to our Terms of Use and Privacy Policy. To begin investing on Stash, you must be approved from an account verification perspective and open a brokerage account.