Sep 21, 2023

What Is Compounding? An Explanation of Compound Interest

The sooner you start putting money away, the more it can work in your favor.

| What does compounded mean? Compounding Definition: Compounding is the returns earned from interest on an existing principal amount, as well as on interest already paid means that, over time, you earn interest not only on your original investment (the principal) but also on the interest that has already been added to the principal. |

If you’re new to investing, compounding should be at the start of any investing discussion. Compounding refers to earning interest on top of the interest you’ve already accumulated from previous periods, and it’s a way to potentially magnify your savings over time just by staying invested in the market.

If you can understand compounding as a beginner, it allows you to get excited about the possibilities of investing and set expectations about how that money can grow over time.

So, what is compounding?

Simply put, compounding is the percentage of money you earn on top of your original investment (aka your principal investment) plus its earnings from previous periods. It can be calculated by banks or financial institutions on a daily, monthly, or annual basis.

How does compound interest work?

Compounding interest is the interest on a loan or investment found by the initial principal plus the interest accrued from preceding periods.

The principal is compounded because it’s periodically increased by a percentage (i.e., adding 10% each month). This differs from linear growth when the principal is increased by a fixed number (i.e., adding 10 each month). Let’s look at an example:

Imagine that you deposited $100 in a savings account that accrues 10% interest annually. After one year, you’d have $110 in that savings account. After two years, though, your interest would have compounded, and you’d have $121.

That’s because you’re not just earning 10% interest on your initial deposit ($100)—you’re earning interest based on your new total earnings ($110). So after two years, you’ll earn your 10% interest based on your new total of $110. Here’s a breakdown of how those earnings could compound over time:

| Year 1 | Year 2 | Year 3 | |

| Starting balance | $100 | $110 | $121 |

| + 10% interest | $10 | $11 | $12.10 |

| Ending balance | $110 | $121 | $133.10 |

Initial deposit: $100

Year 1: $100 + (100 x 10%) = $110

Year 2: $110 + (110 x 10%) = $121

Year 3: $121 + (121 x 10%) = $133

And after 10 years of compounding at a rate of 10%, your $100 deposit would grow to $259.37. That’s the power of compounding in action.

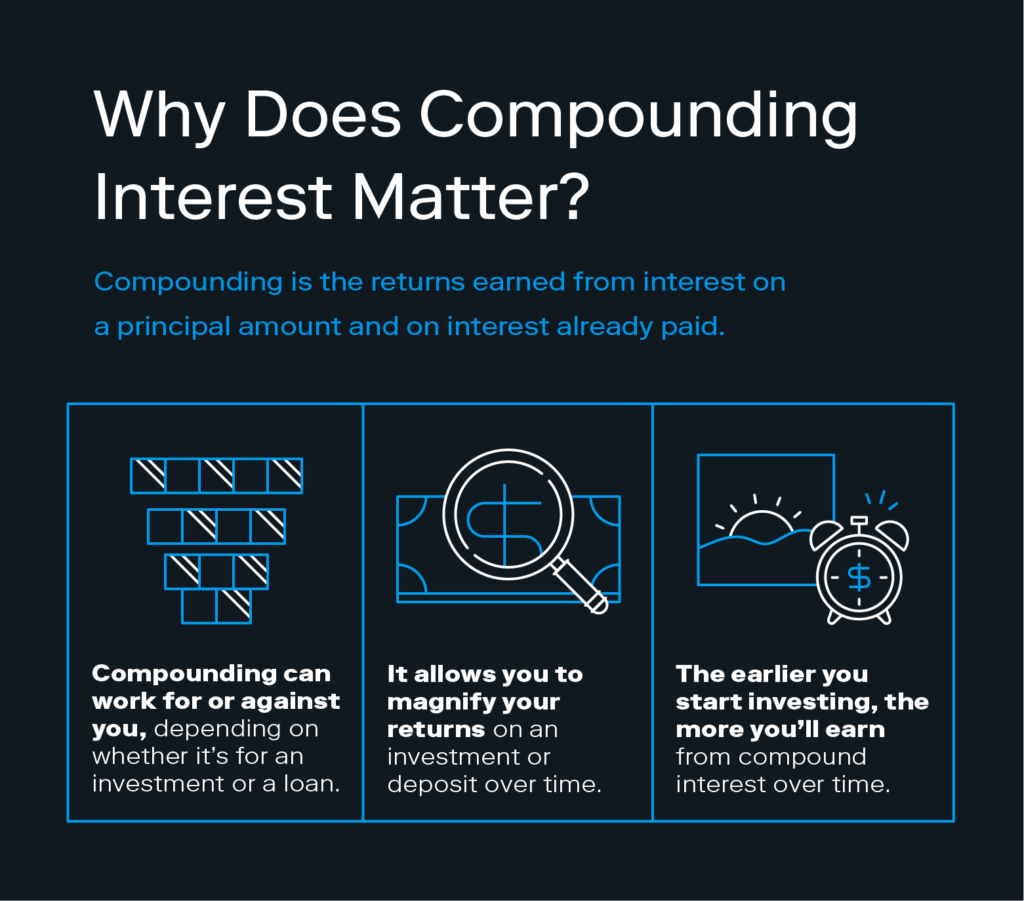

So, what does compounding have to do with you and your money?

Compounding can either work for you or against you, depending on whether it’s for an asset or a liability. The example above shows how compounding works in your favor if it’s for a savings deposit or investment (assets).

But it can also apply to liabilities, like money owed on a loan—when compounding interest is accrued based on your unpaid principal plus interest charged over time. In this case, the compounding interest means the amount you owe increases (compounds) over time. Compounding money when it comes to accounts with debt is something you want to avoid.

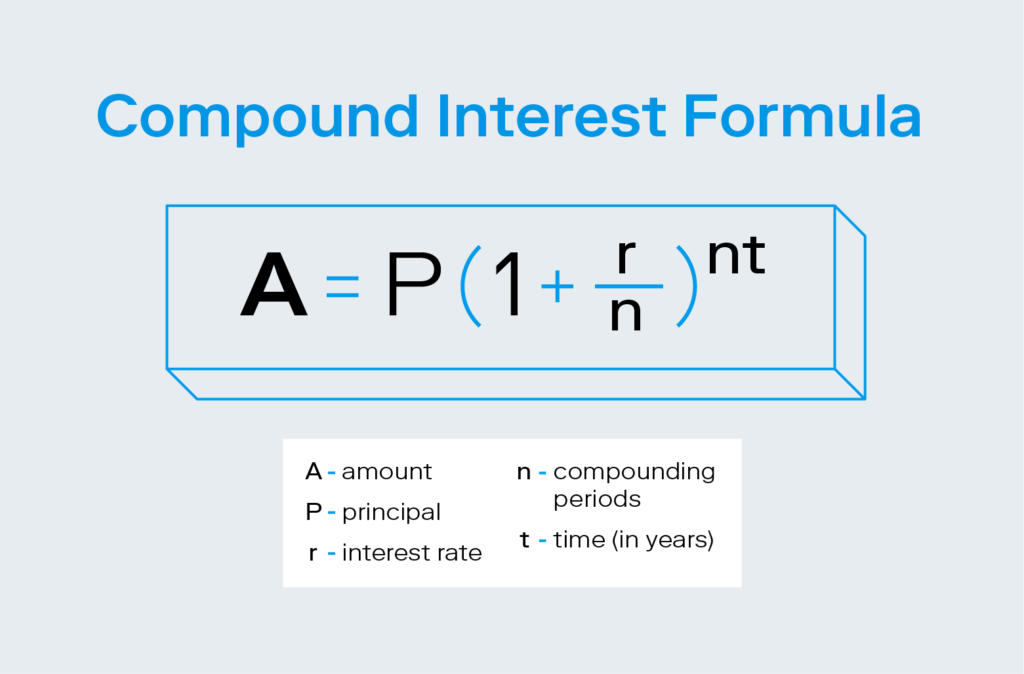

The compound interest formula

The formula to calculate compound interest is A=P(1+r/n)nt.

- A = the total amount of money accrued on your principal plus interest, after n years

- P = principal (the initial investment or deposit)

- r = interest rate (in decimal form)

- n = number of compounding periods (how often the interest is compounded per year)

- t = time in years (how long the principal remains invested/deposited)

Let’s put this formula into action with some concrete numbers. Say you deposit $500 into a savings account with a 5% interest rate that compounds monthly for 10 years. So:

- P = $500

- r = 0.05

- n = 12

- t = 10

Now let’s plug those numbers into the compound interest formula:

A = P (1 + [r / n]) ^ nt

- A = $500 (1 + [0.05 / 12]) ^ (12 * 10)

- A = $500 (1.00417) ^ (120)

- A = $500 (1.64767)

- A = $823.84

In 10 years, your new total is $823.84—your principal plus $323.84 in interest.

Compound interest vs. simple interest

Simple interest is interest that’s paid only on the initial principal of a loan, and not on any interest from previous periods. That means the interest isn’t compounded.

Going back to our $500 savings deposit example, a deposit of $500 with a 5% interest rate would mean earning $25 a year, every year. Instead of the earned interest being added back into the principal (compound interest), simple interest is calculated based on the original principal alone.

Here’s how to calculate simple interest:

A = P (1 + rt)

- A = the total amount of money accrued after n years, including interest

- P = principal (the initial investment or deposit)

- r = interest rate (in decimal form)

- t = time in years (how long the principal remains invested/deposited)

We can see that this formula is just a simplified version of the compound interest formula. Here’s what it looks like using our $500 example:

A = P (1 + rt)

- A = $500 (1 + [0.05 * 10])

- A = $500 (1 + 0.5)

- A = $500 (1.5)

- A = $750

Ten years of earning 5% simple interest on your $500 deposit yields an extra $250 earned.

Compound returns

The answer to “what is compounding” is incomplete until we also understand the element of compound returns. The magic of compounding is revealed when it comes to compound returns on your investments in the market.

When you keep reinvesting the dividends you earn, your returns have the chance to compound significantly over time. And if you’re a young investor who still has a ways to go until retirement, your opportunity to accumulate long-term wealth grows exponentially.

| Investor Tip: Taking advantage of the power of compound returns always comes with some risk. While market fluctuations and periods of downturn should be expected, keeping your principal invested and regularly reinvesting those dividends—regardless of market performance—increases your chance of seeing overall positive returns. |

Timing is everything when it comes to compounding. The sooner you start investing, the more time that money has to grow. Even a small amount a day can add up to sizable returns thanks to the power of compounding. Here’s a brain teaser to prove it:

If you were offered the choice of $100,000 today, or a penny today with the amount you receive doubled every day for a month (a penny on the first day, 2 cents on the second day, 4 cents on the third day, etc.), which would you choose?

Surprisingly, it’s smarter to start with the penny, because by day 31, you’d have more than $10 million. That’s the magic of compounding.

Examples of compounding

As we mentioned earlier, compound interest can work for you or against you, depending on whether you’re investing money or owing money. Here are some examples of compounding in different types of accounts:

- Savings and checking accounts: Making deposits into an interest-bearing account like a savings account means that interest will be added to your balance, allowing your money to grow over time.

- Tax-advantaged retirement accounts (401(k)s and Roth IRAs): Investments in accounts like a 401(k) or a Roth IRA also compound over time, and you can grow your balance faster if dividends are reinvested regularly.

- Student loans, mortgages, and other personal loans: Compound interest works against you when you’re borrowing money. Compounding on loans means any unpaid interest for a given period is added to your loan balance, from which future interest charges are accrued.

Best practices for approaching compound interest

Any new investor should apply the power of compounding if their goal is to accumulate long-term wealth. Use these tips to reap the full benefits of compound interest and allow your money to work for you:

- Start early: The sooner you start investing, the longer your money has to grow. Every day you wait is a missed opportunity to benefit from the power of compounding.

- Pay off debt: Since compounding works against you when you’re borrowing money, prioritize paying down any debts to avoid paying more over time.

- Focus on the long term: Time is on your side when it comes to compound interest. Instead of going after short-term gains or cashing out when the market is high, learn to ride the waves of the market and give your money time to grow.

- Look at APY, not APR: Focus on annual percentage yield (APY) rather than APR when comparing accounts. The APY provides a more accurate view of expected interest earnings, whereas APR accounts only for the simple interest rate.

- Choose accounts that compound interest daily: Compounding frequency is the interval at which your interest is paid out. The more often interest is paid, the greater returns you’ll see from compound interest—look for accounts that compound daily rather than quarterly or annually.

The concept of compounding reveals why investing can be a smarter path to building wealth than simply saving. Not to mention, one of the keys to maximizing your financial potential is to save or invest money early and often.

If you’re looking for extra support, consider turning to a platform like Stash—users can automate the investing process with the help of Auto-Invest, which can save or invest money for you automatically.

Investing made easy.

Start today with any dollar amount.

Compounding FAQs

Have more questions along the lines of “what is compounding?” We have answers.

What is the rule of 72?

The Rule of 72 is a calculation that estimates how long it would take for an investment to double in value as a result of compound interest. Here’s the formula:

Years to double = 72 / rate of return on investment (the interest rate)

In other words, you can find the number of years it would take to double an investment by dividing 72 by the interest rate.

How can investors receive compounding returns?

Investors can receive compound returns through dividend payments. If you’re investing in stocks and the value of a stock grows over time, you can earn compound interest by reinvesting your profits.

If payouts are made in cash, they will need to be manually reinvested in order to potentially earn additional compounding returns. Mutual funds, on the other hand, often offer automatic dividend reinvestments in order to earn compound returns.

What type of average is best suited for compounding?

For investments that have compounding, the time-weighted rate of return (TWR)—also known as the geometric average—is best suited for calculating average returns. It’s able to provide a more accurate estimate of returns by isolating returns that were affected by cash flow changes, balancing out the distortion of these growth rates.

Subscribe

All episodes are available now. You can listen to Teach Me How to Money right here on our site, and via the podcast apps below.

Written by

Team Stash

Related Articles

15 Largest AI Companies in 2024

The 12 Largest Cannabis Companies in 2024

What Is a Traditional IRA?

Saving vs. Investing: 2 Ways to Reach Your Financial Goals

How To Invest in the S&P 500: A Beginner’s Guide for 2024

Stock Market Holidays 2024

By using this website you agree to our Terms of Use and Privacy Policy. To begin investing on Stash, you must be approved from an account verification perspective and open a brokerage account.