Jun 4, 2018

It’s Possible to Become an IRA Millionaire

You don’t need to start out rich to retire with seven figures.

Retiring with seven figures isn’t as far fetched as it sounds.

In the United States, there are now a record-breaking 157,000 people who have saved $1 million or more in their 401(k) accounts. A 401(k) is a type of employer-sponsored retirement account that many Americans have through their jobs.

The problem is that the majority of U.S. workers don’t have access to such a plan, according to a recent survey from Pew Charitable Trusts.

Here’s something else that might surprise you. Individual Retirement Account (IRA) millionaires are more common than 401(k) millionaires.

About 500,000 people have IRAs with a value between $1 million and $2 million, according to the General Accounting Office, which studied the impact of the tax break given to IRA holders on the federal budget in 2014. GAO used 2011 tax data.

Here’s what’s cool about that number of millionaires. An IRA is a retirement account just about anyone earning an income can set up.

Individual Retirement Account (IRA) millionaires are more common than 401(k) millionaires.

401K vs IRA millionaires

Granted, it’s probably easier to save $1 million or more in a 401(k) than an IRA. A 401(k) lets you put away more money–up to $18,500 if you’re under 50, and an additional $6,000 if you’re over 50. And many employers provide a match on funds their employees put away. All that can really add up over time.

IRAs are available to most people who earn an income, letting you put money away in an investment account on a tax-favorable basis. Since there’s no one matching your contributions (and you aren’t allowed to contribute as much as a 401(k), you may have to save more aggressively over time to get to your magic number.

Quick lesson: What’s an IRA?

There are two types of IRA. Let’s start with the traditional IRA.

It’s funded with your pre-tax dollars, so the money you contribute to your traditional IRA can lower your annual tax bill.

As we said earlier, there are annual limits to what you can contribute. You can put up to $6,000 away each year. Once you’re age 50 or older, you can contribute up to $7,000 annually.

After age 59 ½, you can take money from the account with no penalties. By age 70 1/2 you’re actually required by the IRS to start taking money out of your account. This is called a required minimum distribution (RMD).

An RMD is the amount you must withdraw from your traditional IRA starting at age 70 ½. The amount is determined by an IRS formula that comprises life expectancy and account value.

Roth IRAs

The other type of IRA is a Roth IRA. You fund a Roth with the money you’ve already paid taxes on (your net income). Once you’ve funded the account, your earnings can grow tax-free.

Roth IRAs also have yearly contribution limits, meaning you can only put in $6,000. However, like a traditional IRA, if you’re 50 or older, you can contribute up to $7,000.

When you’re age 59 ½, you can access this money without paying a penalty. Unlike a traditional IRA where you are required to begin taking money out of your account by age 70 ½, you can keep adding to your Roth IRA for as long as you like.

The power of compounding and your IRA

Even saving small amounts of money can add up over time, thanks in part to something called compounding. Compounding is earning money on your money, it’s any return earned on your principal, plus your past returns.

For example, if you have money in a bank account, it’s the interest on that sum plus the past interest it has earned over time. If you have money in an investment account, it’s the percentage you may earn on top of your original investment, plus its previous earnings.

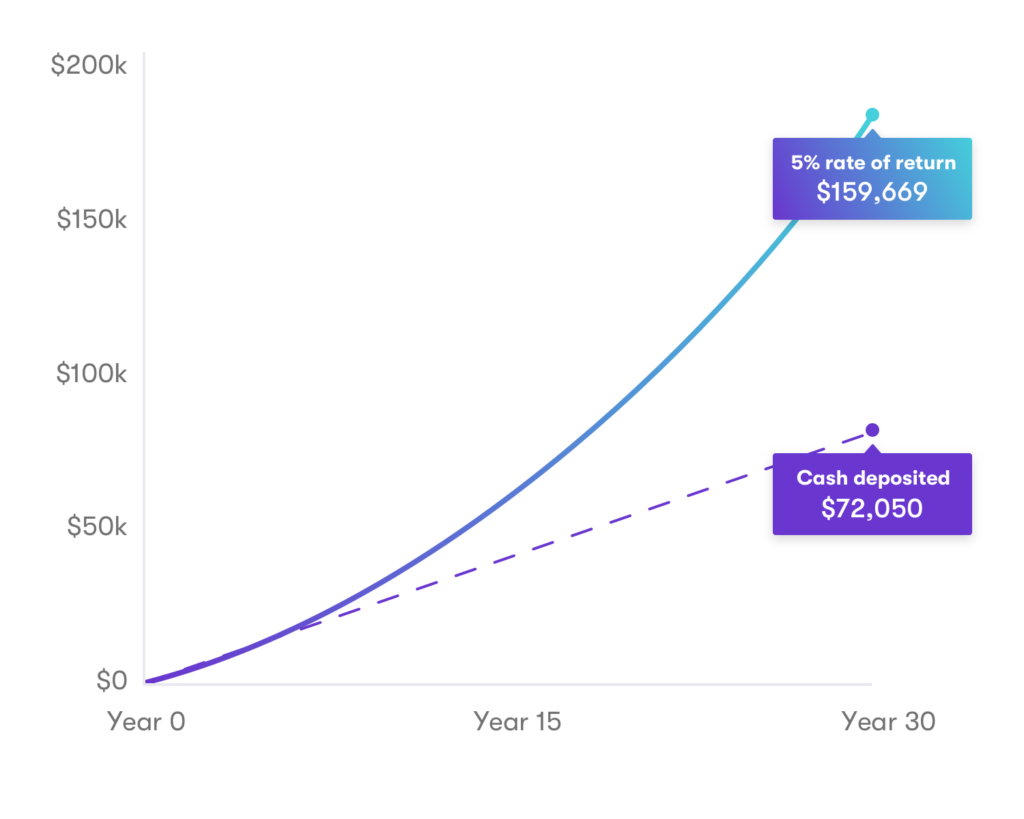

Here’s an example of what compounding looks like, if you put aside $50 a week, or $200 a month for the next 30 years, earning 5% annually. You’d have $159,669. With interest and compounding, that’s more than double the $72,050 of principal you put away.

Make a plan to become an IRA millionaire

If you have a 401(k) through your employer and haven’t set one up, now’s the time to do it. You could be losing out on matching contributions that can really add up over the years.

You can also set up an IRA in addition to your 401(k). The power of compound interest working in two retirement accounts can increase your chances of getting to your magic number

No 401(k)? Anyone can set up and contribute to an IRA. Check out this retirement calculator and learn more about how much you can put aside to get to your million dollar goal.

And that’s how you can really increase your seven-figure retirement chances.

Not everyone will get to the $1 million mark. That’s okay. The important thing is that you try to work saving into your budget and make it a regular part of your financial life.

Subscribe

All episodes are available now. You can listen to Teach Me How to Money right here on our site, and via the podcast apps below.

Written by

Team Stash

Disclaimer: Expected returns or probability projections are hypothetical in nature and may not reflect actual future results.This is a hypothetical illustration of mathematical principles, is not a prediction or projection of performance of an investment or investment strategy, and assumes weekly contributions at a 5% annual rate of return (compounded annually) and does not account for fees or taxes. It is for illustrative purposes only and is not indicative of any actual investment. Actual return and principal value may be more or less than the original investment.

Related Articles

15 Largest AI Companies in 2024

How to Start a Roth IRA: A 5-Step Guide for 2024

The 12 Largest Cannabis Companies in 2024

What Is a Traditional IRA?

Saving vs. Investing: 2 Ways to Reach Your Financial Goals

How To Invest in the S&P 500: A Beginner’s Guide for 2024

By using this website you agree to our Terms of Use and Privacy Policy. To begin investing on Stash, you must be approved from an account verification perspective and open a brokerage account.