Mar 31, 2021

Why Investing Diversification Matters

Reduce risk and volatility, and create global exposure

If you’re new to investing, you’ve probably heard the phrase, “Don’t put all your eggs in one basket.”

The lesson is obvious in the real world—you don’t want all of your eggs to break if you drop the basket. But what does it actually mean when it comes to putting money in the market?

It’s really about the importance of diversification, which is one of the core principles of building a first portfolio. Diversification is also part of the Stash Way, our financial philosophy, which also includes long-term investing and regular investing.

Let’s take a deeper dive into diversification, and we’ll show you why it matters.

Diversification defined

Diversification simply means using your money to invest in many different types of holdings that are not all subject to the same market risks, including stocks, bonds, and cash, as well as mutual funds and exchange-traded funds (ETFs). By diversifying, you can choose investments in numerous economic sectors—not just the hot industry of the moment—as well as in different geographies around the globe.

This is an important concept because diversifying can reduce market risk (volatility) that may subject you to potentially lose a significant amount of money unexpectedly. Keep in mind that volatility exists when it comes to investing and you want to try to navigate your experience as you make progress to accomplish your investment goals.

Let’s take a look at this hypothetical scenario comparing two investors who have constructed their portfolios in different ways, to see diversification in action. We will examine how each of these investors’ portfolios would have performed over the last 20 years.

*Remember all investors are different, and you must take into account your own financial situation and goals when investing. All investing involves risk, and it’s possible to lose money in the market. The Hypothetical below is purely for illustrative purposes and does not represent the actual performance of any client nor does it reflect the performance of any of the underlying investments therein.

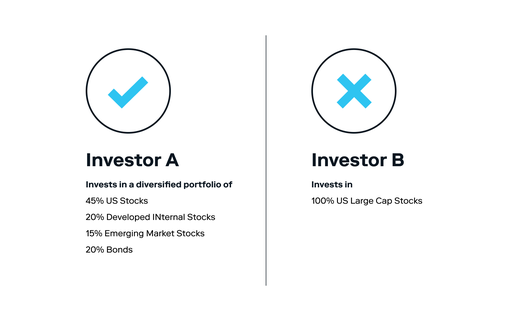

There’s a big difference between the two portfolios, where one investor is more diversified than the other. For example, Investor A has a diversified portfolio that is invested in different asset classes, including stocks and bonds. Likewise, Investor A has invested globally, not just in the U.S., but in developed countries internationally (think of countries including the United Kingdom and Japan), and emerging markets with developing economies, such as India or China.

Meanwhile, Investor B has concentrated investments in the largest companies in the U.S.

You might think that since Investor B has 100% of his portfolio in stocks and Investor A has 20% in bonds, that Investor B’s portfolio performance would probably beat Investor A’s. However, that may not be the case.

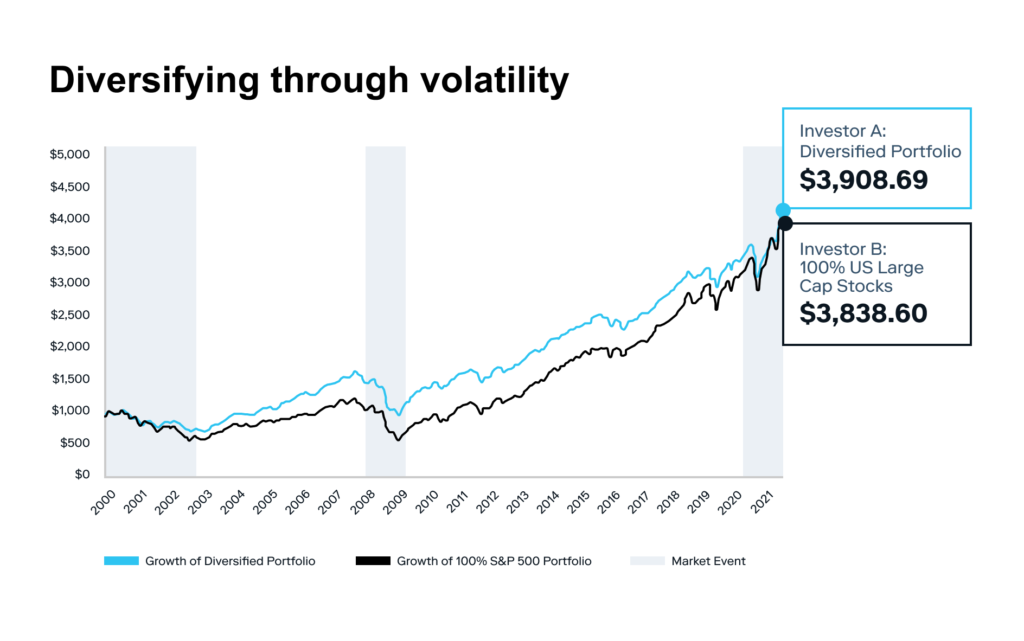

The following chart, which examines what would happen if $1000 was invested in each portfolio over the last 20 years, shows why.

Source: Stash, FactSet as of 12/31/2000-12/31/2020. A diversified portfolio is represented by 45% Dow Jones US Total Stock Market, 20% MSCI EAFE Index, 15% MSCI Emerging Markets Index, 20% Bloomberg Barclays US Universal Index. Assumes portfolio is rebalanced annually. The grey shaded areas represent historical periods where there was market volatility. Past performance is not indicative of future results. You cannot invest directly in the index. This hypothetical does not account for fees or taxes. It is for illustrative purposes only and is not indicative of any actual investment. Actual return and principal value may be more or less than the original investment.

Investor A would have actually beat Investor B’s performance, while meaningfully reducing the overall volatility, or risk, in the portfolio. Why? The answer is diversification.

Many investors have the misconception that if you start adding relatively safer investments like bonds, which traditionally have lower returns than stocks, that your performance wouldn’t be as good.

But that may not be the case. That’s because stocks and bonds have almost an inverse relationship to one another. That means if stocks prices go up, bond prices tend to rise, and vice versa. Bonds can also be typically safer than stocks and can provide an anchor to your portfolio when there is volatility in the portfolio. When stocks plummet, bonds tend to remain steady. We’ve seen this through various financial crises, and most recently during the 2020 pandemic.

Although many investors tend to invest in U.S. companies, because it’s one of the strongest economies in the world, a properly diversified portfolio can also include investments that give you exposure to other areas in the world. Not all countries have the same economic conditions and circumstances, and when there’s an economic crisis, some may even recover faster than others. Additionally, some countries in up and coming markets have greater gross domestic product (GDP) growth potential compared to the U.S. You may want to have exposure to that growth.

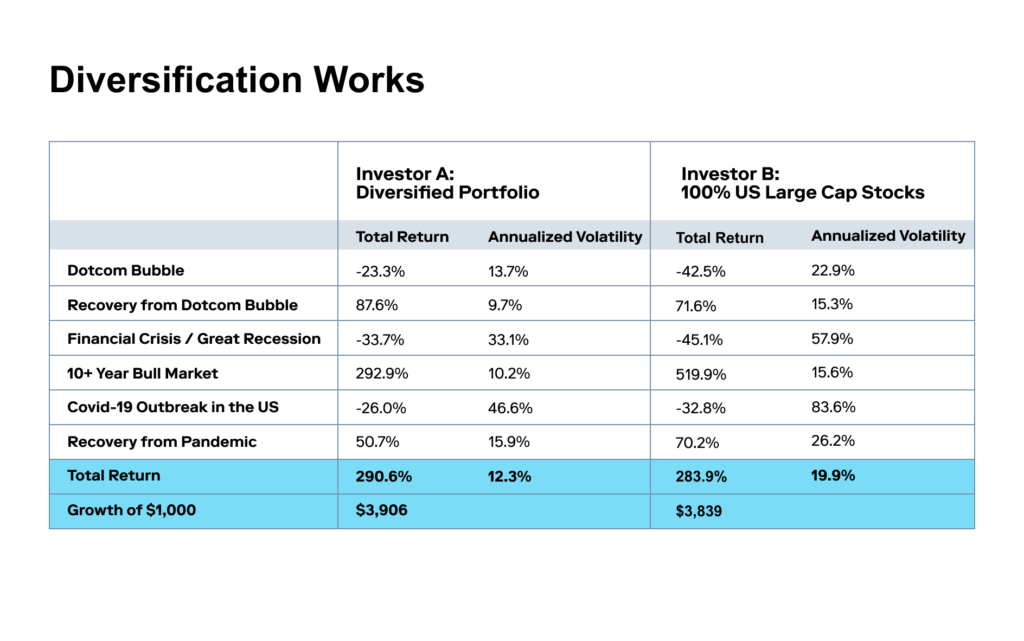

Let’s drill down a bit further, taking a look at significant market events over the last couple of decades to see how each of the portfolios would’ve performed.

Source: Stash, FactSet as of 12/31/1999-12/31/2020. A diversified portfolio is represented by 45% Dow Jones US Total Stock Market, 20% MSCI EAFE Index, 15% MSCI Emerging Markets Index, 20% Bloomberg Barclays US Universal Index. Assumes portfolio is rebalanced annually. “Dotcom Bubble” is represented as the period between 12/31/1999-9/30/2002, “Recovery from Dotcom Bubble” is represented as the period between 10/1/2002-9/12/2008, “Financial Crisis/ Great Recession” is represented as the period between 9/13/2008-3/9/2009, “10+ Year Bull Market” is represented as the period between 3/10/2009- 2/21/2020, “Covid-19 Outbreak in the US” is represented as the period between 2/22/2020- 3/23/2020, and “Recovery from Pandemic” is represented as the period between 3/24/2020- 12/31/2020. Past performance is not indicative of future results. You cannot invest directly in the index.

Although it may not feel like it at the time, diversification can help reduce volatility and the risk of losing money, and may even help a portfolio perform better than a non-diversified portfolio over the long run.

In each time period, with the exception of the recoveries from the 2008 financial crisis and the 2020 pandemic, you can see Investor A’s diversified portfolio actually outperformed Investor B’s, with its concentrated investment in the U.S. stock market. In fact, Investor A’s annualized volatility, which is a measure that shows how risky an investment is, was meaningfully lower than Investor B’s regardless of time period. (12% vs. 20%.) Simply put, Investor A was able to achieve better results, while taking on considerably less risk.

Holding a diversified portfolio does not mean that you can’t lose money. Notice that Investor A still lost money when the Dotcom bubble at the end of the 1990s, as well as during the 2009 financial crisis, and Covid-19 pandemic beginning in 2020. However, Investor A lost less money than Investor B during those times, because Investor A was diversified.

Diversification can help your portfolio weather moments of short-term volatility.

In times when the market is doing well, such as during the last bull market or in the ongoing recovery from the pandemic, it may seem like you’re not making as much money. Shifting your focus to the long-term, having a steady diversified portfolio can help you end up making more than a less diversified portfolio meanwhile exposing you to less risk than a concentrated portfolio. The lesson? Risk reduction does not necessarily have to come at the expense of reduced performance.

That’s why Stash always reminds you to think of the long term, and stick to a portfolio that is representative of your investment goals. Let that drive your investment decisions, not emotions. Diversification, investing for the long term, and investing regularly are all part of the Stash Way, our investing philosophy.

Bottom line: although it may not feel like it, diversification can work through times of volatility and even in up markets. Diversification is one of the investing principles of the Stash Way. We want to constantly remind you to diversify so you are building good investing habits. Note: It’s important to remember that even with diversification all investing entails risk, and you can always lose money in the markets.

Consider a Smart Portfolio

Here at Stash, we have two ways to help you do this.

If you are new to investing or you would like to be more hands-off with investing, we created Smart Portfolios. Our team of investment professionals created portfolios consisting of exchange traded funds (ETFs) that are diversified to minimize risk to help you obtain investment goals. You don’t need to monitor or make any investment decisions, because we do this for you.1

If you rather be more hands-on with your portfolio, we’ve created the diversification analysis tool.2 The tool will take a look at your portfolio and align it towards your risk profile to make recommendations and create guardrails that steer you back on track towards your goals. Diversification analysis only works with Personal Portfolio3 accounts, where you make the investment choices for the stocks, bonds, and ETFs you want in your portfolio.

Subscribe

All episodes are available now. You can listen to Teach Me How to Money right here on our site, and via the podcast apps below.

Written by

Team Stash

1 This type of account is a Discretionary Managed Account. This is a taxable brokerage account that Stash has full authority to manage according to a specific investment mandate. Diversification and asset allocation do not guarantee a profit, nor do they eliminate the risk of loss of principal.

2Stash through the “Diversification Analysis” feature does not rebalance portfolios or otherwise manage the Personal Portfolio Account for Clients on a discretionary basis. Each Client is solely responsible for implementing any such advice. This investment recommendation relies entirely on the responses you’ve provided regarding your risk tolerance. Stash does not verify the completeness or accuracy of such information. Investing involves risk, including possible loss of principal. No asset allocation is a guarantee against loss of principal. There can be no assurance that an investment strategy based on the tools will be successful. Diversification and asset allocation may not protect against market risk or loss of principal. This information should not be relied upon as research. Carefully consider any ETF’s investment objectives, risk factors and charges and expenses before investing. This and other information can be found in the ETF’s prospectus which may be obtained by visiting the ETF’s prospectus pages. Carefully review and consider the information available on the Stash App about each investment recommendation, in any applicable ETF prospectus, and in any applicable public company filing or report before making any investment decision. These investment recommendations are constructed to provide clients with explicit guidance on how to allocate to a globally diversified set of investments for the purposes of long-term investing. Clients make contributions to their Personal Portfolio account and are responsible for directing purchases and sales of specific investments. For clarity, while Stash provides investment recommendations to Clients, Stash does not have authority to execute its investment recommendations on behalf of any Client without such Client’s consent and approval of each specific transaction through the Personal Portfolio Invest account.

The Diversification Analysis is based on a Client’s portfolio composition compared to a suggested allocation. The Diversification Analysis calculates the Client’s overall portfolio diversification and is used to reduce risk by encouraging the Client to diversify further. The calculation is performed by assessing the Client’s portfolio holdings and grading each asset held by its underlying exposures. The asset is graded by qualities such as asset type, regional exposure, and percentage allocation within the portfolio. For each risk profile available on Stash, a desired portfolio allocation is created by the Stash Investment Committee. The desired allocation is used to compare to the Client’s portfolio in efforts to provide advice on how to improve diversification.

3This type of account is a Non-Discretionary Managed Account. This includes a self-directed individual taxable brokerage account whereby Stash does not manage this account on a discretionary basis.

Related Articles

15 Largest AI Companies in 2024

The 12 Largest Cannabis Companies in 2024

What Is a Traditional IRA?

Saving vs. Investing: 2 Ways to Reach Your Financial Goals

How To Invest in the S&P 500: A Beginner’s Guide for 2024

Stock Market Holidays 2024

By using this website you agree to our Terms of Use and Privacy Policy. To begin investing on Stash, you must be approved from an account verification perspective and open a brokerage account.