Jun 8, 2018

Americans are Paying More Than Ever For Their Cars

…Even if it exhausts their budget.

Americans love their cars. Even if they can’t afford them.

New cars, trucks, and SUVs are getting more expensive, as the average U.S. driver opts for pricier models while tightening credit conditions have led to higher interest rates on car loans. All told, drivers are seeing their car payments eat up a more significant portion of their budget than ever before.

The average American is paying a record $523 per month for a new vehicle, according to a report from Experian. That’s an increase of $15, or 3% from last year.

Consumers are also borrowing more than ever to finance their purchases, with the average new vehicle loan now clocking in at $31,455, up $921 from 2017. Those loans aren’t getting cheaper, either. The average interest rate is now 5.17%, up 0.31% from last year.

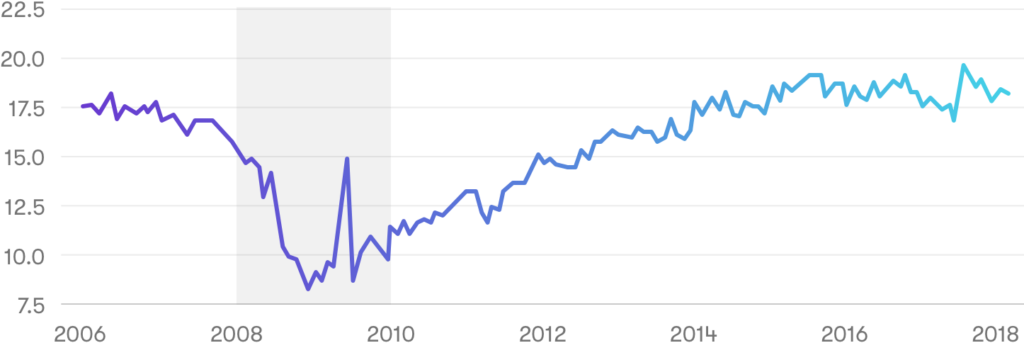

And higher prices evidently aren’t keeping consumers away from dealerships, as Americans are buying cars in droves. Consumers purchased nearly 18 million vehicles in April 2018, according to government data. Compare that to 2008 and 2009, during the Great Recession, when sales weren’t cresting above 10 million.

Why are costs going up?

The average price paid for a new vehicle in the U.S., at the beginning of 2018, was $36,270, according to industry data. That’s an increase of about 4% from January 2017.

The primary, but not only reason that average costs are increasing is that U.S. consumers are gravitating toward bigger, more expensive models. Ford, for example, recently announced that it would be gutting its lineup and focus almost exclusively on SUV and pickup truck production in coming years–vehicles that drive higher revenues.

Auto dealers have even tried to make purchasing smaller vehicles more enticing, offering significant discounts, rebates, and incentives on small and midsize cars over SUVs, according to Autotrader. But consumers are still opting for the bigger, more expensive vehicles.

The best-selling cars in the U.S., for example, are Ford F-Series pickups, followed by the Chevrolet Silverado pickup, according to industry data. In fact, the Ford F-Series has been the best-selling passenger vehicle in America for 41 straight years.

Other reasons that vehicle costs are on the rise? Inflation, regulation and tighter credit conditions are all in the mix. Consumers are also taking on bigger loans, with longer repayment terms. Some people are even taking out auto loans with repayment terms between 84 and 96 months, which can mean that drivers are paying more in interest. The average U.S. auto loan in 2018 is 60 months, at 4.21% interest, according to industry data.

New tariffs could also lead to bigger sticker prices, ranging from an additional $130 to $400, according to analysts.

Operating expenses

Buying a car is one thing. Driving and maintaining it is another–with a whole other slate of expenses for which drivers need to budget. The average cost of owning and operating a car is nearly $8,500 per year, according to data from AAA.

| Average annual ownership costs | |

|---|---|

| Maintenance | $1,186 |

| Gas | $1,500 |

| Insurance | $1,029 |

| Depreciation | $3,571 |

Gas prices have been trending upward lately, too, meaning that operating costs will likely continue to increase.

Can you afford a new car?

Buying a car is a big expense, and even industry insiders are privy to the bind it can create for consumers.

“I think we’re certainly at a point where [automobile] affordability is a question,” Melinda Zabritski, Experian’s senior director of automotive finance solutions, told CNBC recently. “When you look at how much income you need to support that [car] payment, it certainly is higher than your average individual income.”

You may love your car, but that doesn’t necessarily mean you can afford it.

Contrast the average monthly payment of $523 for a new car with what American workers are earning. The median weekly earnings for a U.S. worker in the first quarter of 2018 were $881 before taxes, according to government data.

Factoring in taxes, a monthly payment on a new car can easily eat up a quarter of the average American’s monthly budget, or more.

If that’s the case, buying a new car may simply be out of reach for the typical U.S. consumer–even if they’ve yet to realize it.

Subscribe

All episodes are available now. You can listen to Teach Me How to Money right here on our site, and via the podcast apps below.

Written by

Team Stash

By using this website you agree to our Terms of Use and Privacy Policy. To begin investing on Stash, you must be approved from an account verification perspective and open a brokerage account.