Apr 7, 2020

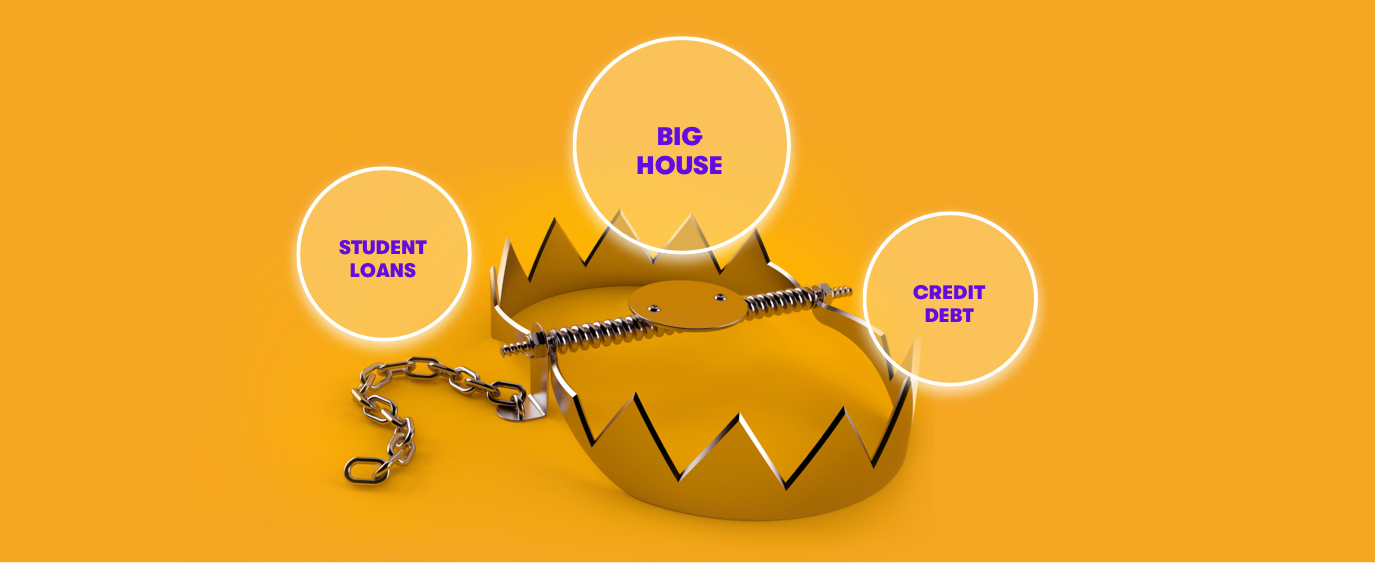

Six Common Financial Traps and How to Avoid Them

Credit cards, payday loans, even timeshares are common money pitfalls.

There’s a financial literacy crisis in the U.S., one that can potentially lead people to make mistakes with their money.

One reason is that personal finance isn’t taught in schools, and as a result, only 16 percent of millennials qualify as “financially literate,” according to a new study by the Teachers Insurance and Annuity Association of America. And a new poll found that only two percent of American adults could get at least five out of six questions correct on a simple personal finance quiz. The survey found that most people had little knowledge about credit and interest.

With this in mind, it makes sense that the average American now carries a record personal debt of $38,000, according to a Northwestern Mutual study. What’s more, the same study shows 87 percent of Americans say nothing makes them happier or more confident than feeling on top of their finances.

So how does such massive debt happen?

Here are six common pitfalls and traps that land Americans in financial trouble:

1. Buying too much house. “People want to be house rich, but end up cash poor,” says Jack Choros, chief marketing officer of Gold IRA Guide, an online retirement planning magazine. “If you can’t put down 20 percent and keep three to four months’ worth of salary in the bank to account for an emergency, your house is too expensive.” Freddie Mac, the Federal Home Loan Mortgage Corporation, has an online calculator to show you what your maximum loan and payments should be based on your down payment and salary. For example, if you have an annual salary of $60K and have $50K saved, you could potentially afford a home up to $244K, with a monthly payment of $1,400.

2. Auto loans that wind up costing more than you expected: Choros’ rule of thumb applies to cars, too. You should be able to put down 20 percent of your car. Unfortunately, more Americans are buying more expensive cars than they can afford. A third of car loans now last for more than six years, according to a recent Wall Street Journal article. Ten years ago, that number was under ten percent. Remember also that cars aren’t great investments. They’re value decreases by 10 percent when you drive it off the lot, 20 percent in 12 months, and 10 percent every year thereafter, according to CarFax. Ideally, you’d be able to pay cash for the entire car, but when that’s not possible, put as much down up front as possible and opt for the shortest loan that’s manageable for you. Choosing a long, 72-month loan over a 60-month loan would cost you hundreds of extra dollars in interest.

3. Carrying credit card debt. The average American has more than $6,000 in credit card debt, according to a 2019 Experian study. This is up three percent from 2018, and can be particularly dangerous because credit cards tend to have very high interest rates. Get serious about debt pay off with methods like the avalanche and snowball.

4. Payday loans. About 2.5 million U.S. consumers take out payday loans each year, according to the credit bureau Experian. These are very high-interest loans–we’re talking up to 400% annual percentage rate (APR)–that are paid back with your next paycheck approximately two weeks after you receive the money. Part of the appeal for consumers is that they’re reportedly easy to get with relatively little by way of a credit check performed by lenders. On top of the high APR, there are also steep processing and origination fees associated with the loans that can push the total APR up to 800%, according to the Consumer Federation of America. Many consumers wind up rolling over loans from one pay period to the next, winding up in a chronic state of indebtedness.

5. Student loans. Student loans are inevitable for so many Americans, and unfortunately there are several ways these loans can trap people.

- Many loans come with a fee. The problem? That fee isn’t discussed at the time of the loan application. Instead, it hits when the loan is transferred. University of Wisconsin alum Chris Mansavage, whom I interviewed, took out student loans in 2012, but wasn’t informed that his loans had a $700 fee that he wasn’t prepared for. Asking about fees is key.

- Your loan may get sold or transferred without your knowledge. If you visit your loan website and see that your balance has mysteriously gone from the thousands to zero, do not simply count this as an act of God. Call your lender. They probably sold your debt to someone else and you haven’t received a notice yet.

- Your loans may not be fixed. In an interview, Lehigh University alum Chris Castelli says he called Sallie Mae after graduation to consolidate his four loans, all of which he had at 2 percent interest. “They advised me not to consolidate, because I already had a good interest rate,” he says. “I was not informed that my interest rate was variable. I fell for it. Soon after, they raised my interest rate above 5 percent. That cost me a ton of extra money over the next decade.”

6. Timeshares. The problem with signing up for and paying for a vacation rental up-front for many years is that you have no leverage if the place turns out to stink, falls into disrepair, or your perfect island getaway is hit by a hurricane and the entire beach disappears. Plus, it’s impossible to sell most timeshares — they’re yours forever. And when you die, they become your heirs’. Perhaps this is why a University of Central Florida study shows 85 percent of people regret buying into a timeshare. A 2018 United States Shared Vacation Ownership Consolidate Owners Report showed 7.1 percent of Americans own at least one week of timeshare of year, and that the industry is growing. The average cost per timeshare is more than $22K with an $980 maintenance fee, according to The American Resort Development Association.

Obviously, borrowing money and making big purchases can’t be 100 percent avoided. But by reading the fine print, asking questions, comparing your options, and staying within your budget, you can avoid these common financial traps.

Subscribe

All episodes are available now. You can listen to Teach Me How to Money right here on our site, and via the podcast apps below.

Related Articles

Credit Cards vs. Debit Cards: The Differences Can Add Up

How To Pay Off Your Student Loans Faster

How To Pay Off Credit Card Debt

What Is the Debt Snowball Method?

Planning Your Finances as a Member of the Military

How to Build Credit: Why You Need It and How to Get It

By using this website you agree to our Terms of Use and Privacy Policy. To begin investing on Stash, you must be approved from an account verification perspective and open a brokerage account.