Apr 7, 2021

Why Your Taxes Might Change if You Worked in Another State in 2020

You could owe income taxes in multiple states.

UPDATE: The Internal Revenue Service (IRS) has extended the tax filing deadline by one month, to May 17, 2021 to accommodate new stimulus payments and a backlog of tax returns. The IRS is also giving individuals who owe money on their 2020 tax returns until May 17, 2021, to make those payments. Individuals can also make contributions to individual retirement accounts (IRAs) for 2020 until May 17, 2021. Due to severe weather, residents of Texas, Oklahoma, and Louisiana have until June 15, 2021 to file, make tax payments, and contribute to their IRAs. Taxpayers who request an extension on the deadline will have until October 15, 2021, to file. You can get more information here.

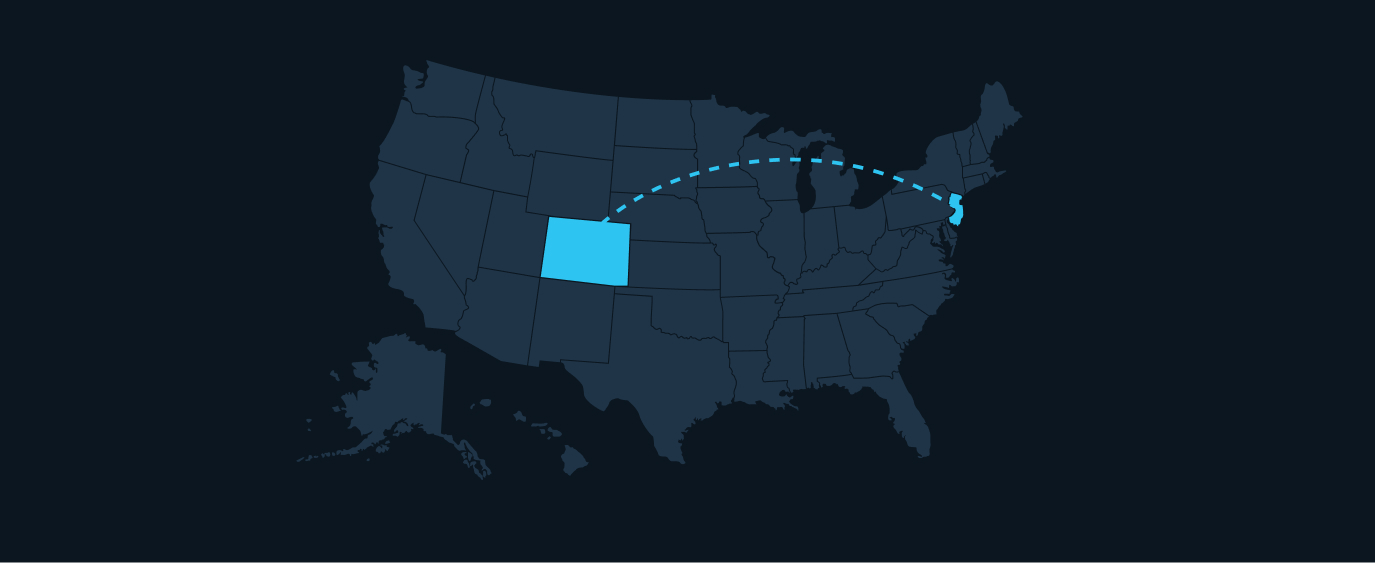

Remote work during Covid-19 has allowed many Americans to move away from the places where they previously lived and worked, even if only temporarily.

Relocating to less expensive locations or to be with loved ones has been one way to save on housing costs and other bills in a year where millions of Americans have lost their employment, or been furloughed. But if you moved out of the state in which you worked during the previous year, keep in mind that you may owe taxes in both of those states, unless they have something called a reciprocity agreement.

As you prepare to file your 2020 taxes, here’s what you should know.

Know the rules in your state

Even if you consider one state your primary residence, once you’ve lived in another state for 183 days or more, many states consider you a resident for tax purposes there. In that case you’re likely to have to pay taxes to that state for the amount of time you worked there, as well as to the state you left. Note that every state has its own regulations, so you should consult with a tax professional on your specific situation.

Taxpayers who do owe taxes in multiple states should likely “file a part year return for each state that indicates the dates that they were in each state, and the income earned in those states,” says Christopher Jervis, an Enrollment Agent (EA) from Lone Wolf Financial in Winder, Georgia.

You should check individual state tax laws, since some might consider you a full-time resident if you’ve been there 183 days or more, says Jervis. “Full-year residents are often taxed on all income, regardless of the state in which it was earned,” Jervis says. However, you might be able to claim a credit or allowance in your state of full-time residence.

Some states might have reciprocity agreements, meaning that you can live in one state and work in another without incurring double taxation. For example, Pennsylvania has reciprocity agreements with Indiana, Maryland, New Jersey, Ohio, Virginia, and West Virginia. So you could live in Pennsylvania and work in Maryland without being taxed twice.

Every state has specific tax laws so you should familiarize yourself with those laws if you’ve moved between states this year. Many, like Florida, have no individual state income tax laws. In fact, six other states—Alaska, Nevada, South Dakota, Texas, Washington, and Wyoming—don’t deduct a state income tax. In New Hampshire and Tennessee, residents don’t pay state taxes on earned income but they do pay taxes on investment income. So if you’ve moved to or from one of these states, you may want to keep that in mind when you file.

Find out which deductions you can take

Itemizing deductions when you’re filing your taxes can be one way to reduce your taxable income. You should familiarize yourself with updated regulations on what may be deductible for you, as allowances do change. For instance, while taxpayers were once able to itemize moving expenses, most no longer can because of the 2017 Tax Cut and Jobs Act. “In order to deduct moving expenses on your federal tax return, you must be an active member of the US armed forces (or a spouse or dependent) moving related to a permanent change of station,” says Josh Zimmelman, the managing partner of Westwood Tax & Consulting in Rockville Centre, New York.

Talk to your human resources department

As of July 2020, 22% of American adults said that they moved or know someone who moved as a result of the pandemic, according to a Pew Research Group survey. If you’ve moved, you may want to speak with whoever is in charge of payroll at your organization, if you haven’t already done so. You can update them on your new address so that the correct deductions are being made to your paycheck, and they can provide you with the right W-2 tax forms for filing.

Doing this can “avoid confusion and can even be used for a tax saving advantage,” depending on where you moved, says Sam Otto, a Certified Professional Accountant (CPA) from Uncle Sam’s Accounting in Helenville, Wisconsin. Otto cites Florida as an example since the state has no state income tax. In that case, moving to Florida and changing your residence might save you money in taxes.

File as soon as possible

Whether you moved in 2020 or not, you should aim to file your taxes as soon as you can. Employers are required to provide their workers with W-2s and other tax forms needed to file by February 1, 2021. Once you have that and any other relevant paperwork, you should be able to file.

“One thing that every taxpayer should expect, whether they moved or not, is a longer than normal turnaround to receive refunds. We expect tax processing to be very slow this year, with refunds possibly delayed due to the nearly nine-month backlog that the IRS is still working on for 2020,” says Jervis. So filing your taxes in a timely manner could help you see a return more quickly if you receive one.

With your Stash account, you can set up Direct Deposit and have your tax refund deposited directly into your account. You might save that refund in a partition for a certain goal, such as buying a house, or use it when you invest.

Subscribe

All episodes are available now. You can listen to Teach Me How to Money right here on our site, and via the podcast apps below.

Written by

Team Stash

Disclosure: This article should not be construed as Tax advice. Please consult a Tax professional for additional questions.

By using this website you agree to our Terms of Use and Privacy Policy. To begin investing on Stash, you must be approved from an account verification perspective and open a brokerage account.