Sep 20, 2018

Investing vs Gambling: Why They’re Totally Different

Why investing can be a better way to build wealth over rolling the dice or scratching a lottery ticket.

Think investing is the same as gambling or scratching off a lottery ticket?

Many people are nervous about putting their money in the market and hesitate because they believe that investing has more to do with luck than anything else.

In other words, they believe their ability to earn a return on their investment comes down to pure chance—like the flip of a card or roll of the dice. Investors and gamblers do have one thing in common: They both want to put more money in their pockets.

Investing vs. gambling

Investing and gambling could not be more different.

| Investing | Gambling |

|---|---|

| You control your risk. You can invest according to your goals and timelines: Conservative, moderate or aggressive. | Risky. The odds are always in favor of the house. |

| Strategy: Slow and steady. Investors plan to make a consistent return on their investments every year. | Strategy: Fast money. Gamblers bet it all for the chance to make a bundle fast. |

| Taxes: By putting your money in a retirement account, you can defer paying taxes on your investment earnings. | Taxes: You have to pay taxes on any gambling or lottery winnings over $600 |

Here’s why investing your money is typically a better option for those looking to increase their wealth, rather than buying a lottery ticket, or going all-in with a pair of jacks:

The odds are in your favor

Anyone familiar with gambling has likely heard the phrase “the house always wins.” Since casinos are in the business of making money for themselves, that means the scales are tipped in favor of the dealers.

Investing is generally a much more effective way of making your money work for you. And most importantly, investors have a lot more control in where your money goes and how it can grow.

Gamblers hope for a quick win. Investors want to build wealth over time

For example, if you bet $1,000 that the roulette wheel hits your lucky number, you’ve got one shot at cashing in. Your odds? 35 to one. That’s a risky bet. And there’s a good chance you’ll walk away from the casino with less money than when you walked in.

Understanding risk

Investing involves risk. But by building a diversified portfolio with stocks, bonds, and holdings from multiple sectors (tech, energy, etc.), you can balance out your risk. In other words, you’re not betting it all on one investment—or putting all of your eggs in one basket.

If one investment goes down in value, you’ll have other investments that may hold steady, and keep your portfolio afloat.

For example, numerous advisers say an effective way to manage your money is by applying aspects of Modern Portfolio Theory (MPT). Nobel Prize-winning economist Dr. Harry Markowitz conceived the idea for MPT which formed the foundation for portfolio management by balancing risk and return.

The general idea of MPT is that by investing in a diverse assortment of stocks, bonds, and other securities in a multitude of countries, you can minimize risk.

Invest with a plan

You’ve probably seen news reports about people who win a lot of money at the casino or by playing the lottery. These make it seem like a lottery win is not only possible but probable. Unfortunately, it’s not. Losing is nearly inevitable when you gamble.

Gamblers hope for a quick win. Investors want to build wealth over time. Fast money sounds great but it isn’t an actual plan to get you to your goals.

Rather than just “win big,” many investors have a specific plan as to what they’re investing for in the long term. This goal, whether it’s saving for a down payment or a child’s college education, should align with your investment strategy.

Once you have a plan in place, you can adjust your portfolio according to your timeline.

The power of compounding

By choosing to invest your money with a solid strategy you can allow your assets opportunity to compound over time.

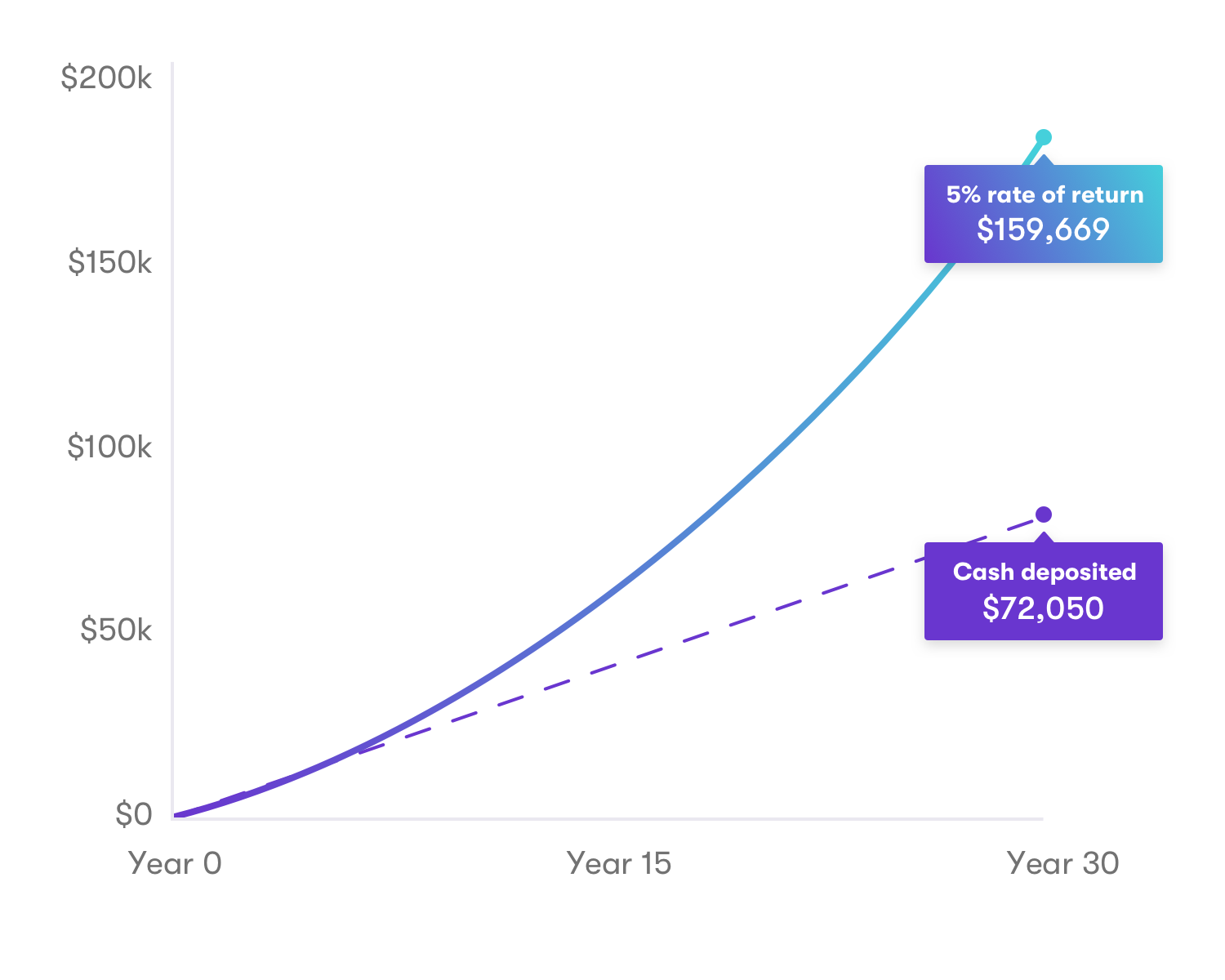

Here’s how compounding works:

Say you start putting away $50 a week in an investment account that owns a variety of stocks, bonds, and cash. If that account earns an average of 5% annually, you’ll have over $159,669 in 30 years when the interest is compounded annually.

Subscribe

All episodes are available now. You can listen to Teach Me How to Money right here on our site, and via the podcast apps below.

Written by

Team Stash

Disclaimer1 The rate of return on investments can vary widely over time, especially for long-term investments including the potential loss of principal. For example, the S&P 500® for the 10 years ending 1/1/2014, had an annual compounded rate of return of 8.06%, including reinvestment of dividends (source: www.standardandpoors.com). Since 1970, the highest 12-month return was 61% (June 1982 through June 1983). The lowest 12-month return was -43% (March 2008 to March 2009). The S&P 500® is an index of 500 stocks seen as a leading indicator of U.S. equities and a reflection of the performance of the large-cap universe, made up of companies selected by economists. The S&P 500 is a market value weighted index and one of the common benchmarks for the U.S. stock market.

Related Articles

15 Largest AI Companies in 2024

The 12 Largest Cannabis Companies in 2024

What Is a Traditional IRA?

Saving vs. Investing: 2 Ways to Reach Your Financial Goals

How To Invest in the S&P 500: A Beginner’s Guide for 2024

Stock Market Holidays 2024

By using this website you agree to our Terms of Use and Privacy Policy. To begin investing on Stash, you must be approved from an account verification perspective and open a brokerage account.